“Gold is Money, Everything Else is Just Credit” - J.P. Morgan

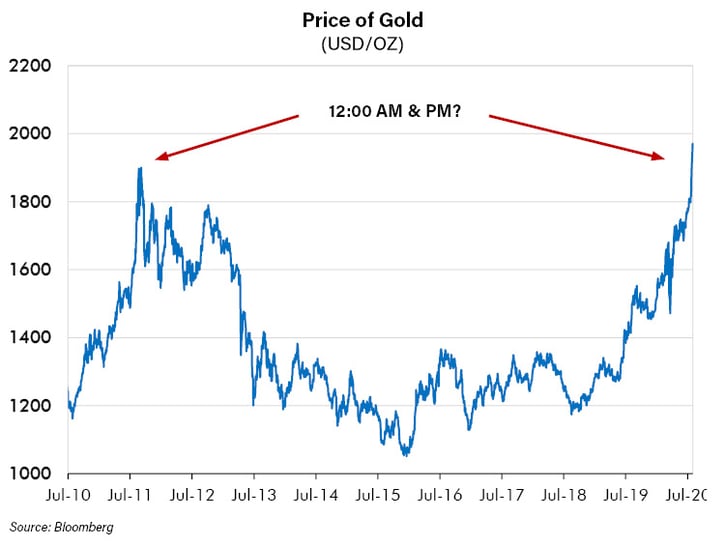

This week the price of gold exceeded its 2011 all-time high of $1921 per ounce. This is an important milestone for our research department. With the old high now eclipsed we are going to explain in detail our thesis on gold in a two-part Risk On / Risk Off. This first part will delve into gold’s relationship to the money most of us think of as “money,” central bank created money, such as the dollar or the Euro. In the second part to be published in two weeks we will examine the ancient shiny metal’s relationship to interest rates, the dollar, property rights and equity prices.

The nearly nine years since the last peak of the gold price was a good part of the prime of my life. It was the entirety of my sons’ teenage years. I went from being the father of a young family to being an empty nester. I enjoyed my professional endeavors during those years, especially the years I’ve spent building out our investment research effort. However, during the entire time, I’ve been bullish on gold. That view and the reasons behind it have been a central underpinning of my understanding of economics and finance. So, watching gold decline for 4 years from 2011 to its ultimate low in 2015 was painful. The grind back up since then has been slow with lots of fits and starts. The emotional toll has been tough because it is hard to be “wrong” for a long time, when sometimes wrong is really just “early,” or as I prefer to term it “un-naturally far-sighted.”

Early in my career, it seemed to me and many of my peers - naively so as it turns out - that whether someone was a good investor could be proven by their most recent or most vocal investment thesis. At several of the firms for whom I worked, the culture was highly competitive and aggressive. Often there were heated debates on investment themes or positions. A typical response from the one who was proven wrong by the market was not to admit error or misjudgment but rather to argue that luck was the primary driver. Often one would hear “a broken clock is right twice a day” when describing the analyst whose supposedly flawed reasoning resulted in the unexpected outcome. The phrase was funny because it was true …. a broken clock is right twice a day.

Luck does drive some success on Wall Street. Great thinkers have written entire books on the subject. “A Random Walk Down Wall Street” by Princeton Economics professor Burton Malkiel is probably the most famous. My favorite is Nassim Taleb’s (of Black Swan fame) “Fooled by Randomness” which argues that many outcomes in life, not just in investing, are falsely attributed to skill when they are in fact due to luck.

So, is gold’s new all-time high an example of the “broken clock” of our research department having the right view in 2011 and now, 9 years later in 2020 due to sheer luck? Nine years is a long time to wait for the hands of the clock to come back around. Or, has our thesis finally been proven right? Only time will tell for certain. We thought that, below, we would make the case that we are still in the very earliest of innings of an unfolding gold bull market.

What is Money?

It is difficult to dispute that Gold has over long periods of time been the most stable easily fungible store of value known to man. Is money’s primary role not, first and foremost, a fungible store of value? Perhaps the simple and most powerful example is this: A gentleman’s tailored suit that Nathan Rothschild might have purchased on High Street in London during the Napoleonic wars costs the same one ounce of gold his descendants would pay for a similar suit today. Those who held their wealth in pound sterling or even United States Dollars would not be able to afford that suit at the same currency value 200 years later, not even close. Why the difference?

Gold is, arguably, the only real money because it is an asset that is no one’s liability and therefore has no counterparty or default risk. Also, and perhaps more important, its supply is finite – meaning limited. The United States Dollar, the world’s reserve currency, while it arguably does not have nominal counter party risk, it certainly is not finite. The Federal Reserve Board (the FED) has the power to produce as many dollars as it pleases. So, in the long run, we think the dollar’s value is dependent on the FED limiting its supply.

Monetarism and its Fatal Flaw

Monetarism and its Fatal Flaw

Has a money system where the form of money is someone else’s liability or is not finite, ever worked in the past? Not that I know of – not in the long run anyway. Such an experiment failed when in pre-history on some island the inhabitants decided to use seashells as money and the islanders realized they could walk the beach picking up seashells and get rich! And so, it would fail again, in similar permutations since then.

In 1994 I was a student at what was then known as the University of Chicago’s Graduate School of Business (now known as Booth). There I studied monetarism, walking the hallowed halls consecrated by monetarism’s founder, Milton Friedman and lesser founding fathers such as George Stigler and others who taught there. Monetarism is, in fact, known as the Chicago school. I was never comfortable with this theory for one simple reason. It assumed a group of “wise men or women,” ostensibly the FED, would not let politics, self-interest or other pressures influence their decisions about keeping interest rates at the “right” level and money finite. But hey, who was I, a 29-year-old neophyte, to question the certainty of monetarism in its most holy shrine?

Could human nature and thousands of years of history overpower those elegant theories? Can it be an accident that the Chicago School rose to prominence right around the time Nixon closed the gold window, an event about which we wrote the last Risk On Risk / Off Report entitled simply “1971?” These academics gave Nixon all the intellectual cover he needed to make his move. Academics and economists from both sides of the political spectrum have been supportive of the demise of the gold standard ever since.

Maybe, at bottom, our bullish thesis on gold is as simple as this: the inability of human beings to withstand the temptation to create money out of thin air. I mean, who would not revel in this power? What does the record show about mankind’s ability to avoid this great temptation of “free” money creation?

So far, to us, the track record is clear. Since at least 1987, whenever confronted with a weak economy, the FED has chosen to lower interest rates or simply just create more money from nothing. The term “Quantitative Easing” (QE) is an Orwellian way of saying money printing, plain and simple. There are many who argue that what the FED has done since the 2008 crisis is good and necessary. We do not disagree. The FED has created a situation where there is so much debt and such precarious financial structures that, if the FED does not print money, there is a risk of total collapse. However, printing money has created a “least bad” outcome, not necessarily what we would consider a good outcome. I am not sure what children are taught these days, but back in the 1970’s when I grew up, here is how it worked. Parents exhorted their children to be frugal. After all, money “did not grow on trees.” Can we say the same thing today? What we call money, the United States Dollar, or the other fiat currencies, appear to grow on trees (or rather grow on a central bank’s balance sheet). Then is it really money? The parents of my generation would not have thought so nor would, J.P. Morgan according to his quote above.

Gold’s Relationship to Central Bank Money Creation

Which gets us back to gold. Make no mistake about where we stand: gold is money. When the central bank creates too much of their kind, gold appreciates. As is illustrated below, the recent story of gold’s appreciation in dollars follows the growth of the central bank balance sheet and expectations surrounding it.

During the late 1990’s and early 2000’s, Alan Greenspan was the Chairman of the FED. His reign was characterized by falling interest rates and accelerating the growth rate in the FED’s balance sheet, although it is hard to see on the chart given the scale of the growth during and after the 2008 crisis. It is our opinion that the anticipation of that crisis and the money printing necessary to alleviate it, sent gold higher at that time, especially starting with its powerful move in 2006.

Then what happened? Why did gold decline for four straight years even though the central bank’s balance sheet kept growing through QE? It is our belief that it was due to the erroneous expectation that the balance sheet growth was “temporary” and would soon be reversed. Gold went into its steepest decline in early 2013 when the FED became very vocal about “tapering” QE. This culminated in the “Taper Tantrum” of that spring which, coupled with the European Financial crisis, caused the FED to abandon tapering and begin QE again.

However, for a time the gold price nonetheless continued to fall. In early 2014 both the gold price and the FED’s balance sheet stabilized (although gold meandered down a fraction more to its ultimate low in 2015) for the next few years as many investors expected QE to end and tightening to begin (Quantitative Tightening or QT). We thought the high levels of debt would not allow that tightening to happen and any attempt at it would slow the economy and force the opposite to occur. We remained bullish on gold throughout the period. After the FED’s brief and failed attempt at QT, we were proved correct: QE came back beginning in the fall of 2019 with a crisis in the REPO market and the gold upcycle began anew. It seems to have really taken off now that a second very large stimulus package to fight the COVID-19 recession is being discussed in Washington. It will likely be financed by more money printing.

Conclusion

Gold has been a linchpin of many, if not most monetary systems since ancient times. Its use periodically becomes controversial, such as with the dollar-based gold standard during the middle part of the twentieth century, especially when inflation is helpful to the establishment in power. As for today, I know of no other time in history when gold’s rejection as money by the establishment has been stronger. Nevertheless, we believe the reasons why gold was needed as money over time is now clearer than ever too. The good part is that gold can act as money whether or not it is official “money”. It can be owned as a store of value that is easily fungible regardless. Additionally, investors can benefit from growth in its demand as money by owning mining or royalty companies in the sector that could appreciate in that scenario.

In our opinion, central bank money has led to debt growth and other imbalances. Yet there is no sign to us that the forces that caused this are being addressed. In fact, we argue the solutions are what caused the problems and therefore they are intensifying. For this reason, we believe the gold market is in a bull market and will remain so for a long time, albeit with many scary corrections along the way. In part II of this publication we will argue that current trends in interest rates, the dollar, property rights and equity valuations are all supportive of our expectation for higher long-term prices. Stay tuned!