The industry agrees that the best portfolios are diversified right? What does diversified mean to you? For most, it means a portfolio of securities like stocks and bonds. In an effort to mitigate risk, many will package stocks and bonds in groups through mutual funds, ETFs, or engaging a professional manager like many of you reading this article have. Across my years in the business, I have run across many clients who sought further diversification through either commercial or residential real estate. Most folks appreciate the monthly income and the availability of certain key tax advantages. Others loathe constant repairs, property damage, and tenant drama. For my part, I have seen as many clients who regret having rentals as love having them and wish they had more. The focus of this installment of Wisdom In Wealth is to have looked at rentals and offer some perspectives on the risks of rentals and how to structure ownership, so those risks may be mitigated. The simple hope here is to make a good thing that much better. Let’s first examine the risks of the rental markets.

Contamination

The first risk is contamination. No, I don’t mean radiation or asbestos, I mean ownership. When we look at a person’s total worth, we must consider everything a person owns as being in one pool. Your cars, art, insurance, bank accounts, business interests, rental property, and anything else titled directly to you are lumped together in your name. As such, most of them may be accessed by creditors, judgments, or legal proceedings. Thankfully, your retirement accounts and Florida homestead are usually exempted from such attachments. It is shocking to learn that a simple car wreck involving your teenage children can spill over to your business or rental interests. Because you own all the cars in the family along with other assets this creates an access point to the other assets titled to you. This is also one of the key reasons that I recommend against sharing a joint account with aging parents, or growing kids. Your assets can become attached to their legal or credit issues because of the keyhole created by the joint tenancy.

Probate Risk

Second, is probate risk. As I have discussed in several of the recent Wisdom in Wealth posts, any state where your family owns real property or certain business interests will require your estate to file probate. If your real property is spread over more than one state, the subsequent probates are referred to as ancillary probate. Thankfully probate matters are creatures of state law. So, they are to some extent contained in the state where they originate. Probate is usually a slow, arduous, public, fee-rich proceeding. In Florida, the state code allows for attorney fees at a rate of 3% of the estate plus expenses. Having to ask your family and attorneys to deal with the high costs, and differing rule sets for multiple probates is not a desirable outcome. Oftentimes, low-liquidity assets like rentals or businesses may have carrying costs that can starve an estate of badly needed liquidity. The further the estate extends, the longer the process may take before your family can find closure and settle final affairs. Smaller, tighter, and faster are all good goals to reach for in this case.

Lawsuit & Liability

Third I want to discuss the obvious liabilities of rentals which are lawsuits and liability. Injury, negligence, and death that occur on your property can often create long, slow, expensive lawsuits. Someone very wise who works with us at CWA said to me, “Anyone can bring a lawsuit, so long as they can find an attorney to represent them…they don’t have to be right”. Sadly, in today’s world people tend to be all too happy to create such suits. As discussed above, if you have more than one rental or business titled in your name, the whole group is at risk from any one of the parts. A simple slip-and-fall injury judgment in one property can be based on the group’s values. Say you have four properties valued at a total of $2.3 million dollars and the injury occurred in the least expensive of the group. Even though this property is maybe only worth $150 thousand dollars, the judgment can reach into values of the other homes or assets titled to you outright. This kind of judgment could be catastrophic to your family finances.

Family Legacy Issues

Finally, I want to discuss a more tender topic which is family legacy issues. Families are all the same. They are a collection of heart-racing victories and gut-wrenching failures. They are full of colorful children and grandchildren with their own ideas about how things should go. Today families are more blended, multiracial, genderfluid, and non-traditional than at any time in history. So, if parents have a host of business and rental properties, how do they divide them up in the estate? Do the heirs want the benefits and liabilities of owning rentals after inheritance? Would they prefer a sale and cash payment? Is living in an inherited rental an option? How do you protect your interests, and guide your heirs in protecting theirs? Would it make more sense to consider leaving the group of properties as a family income stream for generations? Very few of these questions have a simple answer. They all require thought, consideration, and discussion at the family table as well as with your professional staff like attorneys, CPAs, and financial advisors. The greatest care must be taken to treat heirs fairly albeit not equally and see what is the greatest good for the family.

Now that we have discussed the risks of contamination, probate, liability, and family, let’s talk about how to address these issues. First, and likely most simply we suggest having proper insurance. Umbrella insurance is commonly very price effective. You can buy quite a lot of coverage for a few dollars per year. Obviously, cost and value are relative terms, but given the risks above, we highly recommend an umbrella policy and a needs analysis on your liabilities. Having a policy like this can give your family critical liquidity to satisfy a judgment against you. Otherwise, your family may be forced to fire-sell assets to cover judgments and legal fees. I have not met a family yet who was excited at the prospect of such a sale. CWA does offer this kind of coverage and we’d be happy to discuss the pros and cons with you. Each family has special considerations and should be treated accordingly.

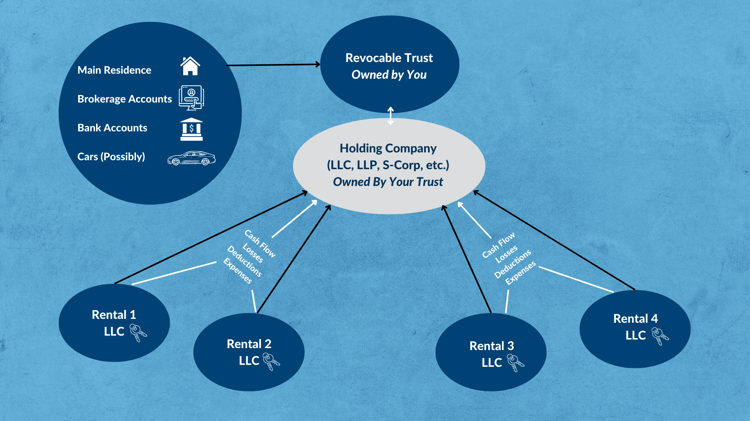

After you have proper insurance coverage for your liabilities, we strongly suggest developing separation and encapsulation of your family’s individual interests. Legal judgments, attachments, and creditors can only attach to what is available. So, we must orient things to control that availability. In an estate planning course I took, the attorney who taught it said, “Control everything and own nothing”. I am not sure I agree with owning nothing, but by not directly owning things we create divided assets. Entity ownership is often the very best solution to many of these risks. If you title your assets into entities, the entity owns the property, not you directly. This may seem confusing at first but stay with me and I will explain. By creating entities such as sub-chapter S-corporations, C-corporations, LLCs and titling property to them, you can insulate each item contained in the entity from other items that may be titled to you. So, each entity’s liabilities start and stop with that entity. By having 4 rentals each contained in their own LLC, they can be insulated from each other and your personally titled property. The entity can take on a few forms based on your attorney’s preferences, but the overriding concept here is to break up the ownership liability into smaller pockets that protect you and your properties from judgments and ancillary probate. There is a good deal of debate over the best structure for multiple rentals. As usual, I suggest garnering the support of appropriate legal counsel, but I would like to suggest a framework as an example of one way we have seen success in.

Source: CWA

Source: CWA

How it Works

By setting up a revocable living trust to own your personally titled assets you can limit probate costs and have high control over the mechanics of your estate. Then by encapsulating each of your rentals, you limit the liability of each to itself. Then in between your trust and LLC’s you can have another LLC/S-corp to behave essentially as a holding company. That entity holds title to your rentals and further separates your interests. You now have at least two layers of separation. The assets are separated from each other, and you are separated from them. All of the cash flows, losses, depreciation, and other associated comings and goings all flow up to the holding company and then on to you. This strategy is on the complex side, but it does serve to shield the whole from any of the parts. I will go on from here to discuss a few items of note.

I use titling words here like subchapter S-corporations, C-corporations, Revocable trust, Holding company, and so on. These are words used to imply mechanics. They are not the only options. Your situation or legal counsel may very well suggest other words of mechanic to you based on your unique family, holdings, or state of main domicile. CWA always suggests having appropriate counsel while using this discussion as an example of one way to achieve your family’s goals and mitigate the risks listed above.

You may want to ask your CPA about having the Holding Company LLC you create behave as a subchapter S-corp. LLCs and subchapter S-corps treat income differently because of a special Qualified Business Income pass-through deduction. This deduction is going to sunset in 2025, but in essence, the subchapter S may be able to save up to 20% on certain types of income. This is a complex sequence event and is outside the scope of this discussion, but it is worth research and discussion with your tax professional.

The final thoughts of this discussion are about legacy planning. As stated above, families are all made up of colorful people in all kinds of situations with all kinds of relationships with each other. If your family owns a group of properties that you want to stay intact for future generations, you should consider creating divided interests. Setting up your holding company structure as an LLC, Family limited partnership (FLLP), or other such entity, the senior owners may be able to gift, sell, or bequeath a minority interest in the group of properties as a whole. There are certain valuation methodologies that can favorably impact the gifting or sale of such interests. By thinking of it this way, you can decrease the ownership and income stake you have in the group while shifting those interests to other family members. Doing so may ensure that you do not have to select certain heirs to receive title to certain properties. Hopefully, this limits the sometimes-harsh feelings of inequality across your family. If you create these minority interests while you are alive, you may retain the controlling interest and leadership role. After estate settlement, the family could then move into group ownership where they all have beneficial interests, but no singular title to the property. Hopefully working together in stewardship over a dynastic group of properties and incomes.

As always, our goal is to give food for thought on topics that can be complex to think through. The topics usually have long-reaching and complex repercussions and may require legal, investing, and tax support to execute. If this topic piqued your curiosity or created questions about your family structure, please reach out to us. We would relish a chance to consult with you.