“The holy passion of Friendship is of so sweet and steady and loyal and enduring a nature that it will last through a whole lifetime, if not asked to lend money.”

-Mark Twain - Pudd'nhead Wilson's Calendar

Frequent readers of this weekly know that we write often about credit. Credit sounds like a complicated financial term but it’s really quite simple. It’s about lending money. The borrower promises to repay the money he borrows at a certain date, with interest payments all along the way to the lender. The bond market is just a more formal version of this simple lending transaction, with the added bonus that these bonds, these ‘lending contracts,’ may be bought and sold between investors who were not initially party to the deal. This week’s Trends and Tail Risks is devoted to describing how we invest in bonds. Our job as investors is to identify the risks for which we are best compensated and that have the largest margin of safety. Sometimes this means taking credit risk. Other times this means taking duration risk. We invest in bonds to make money - not to hide! This week we explain how we do so.

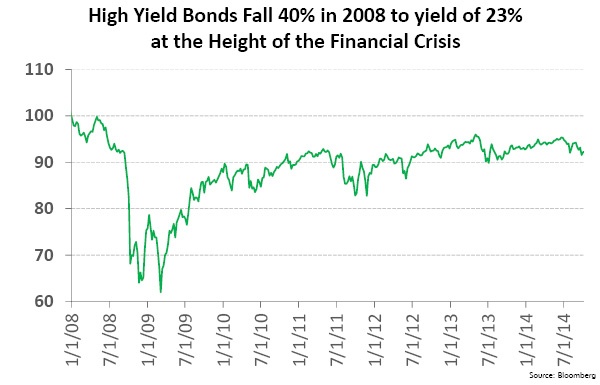

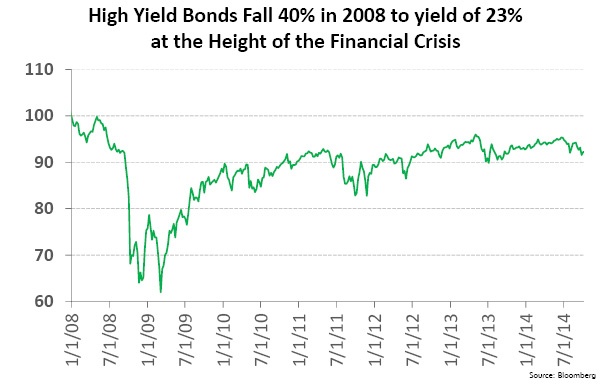

High Yield Bonds Do Not Diversify an Equity Portfolio

If they are not careful, investors may fall into the trap of relying on an overly simplistic model of lending where returns are simply a function of credit risk. Higher risk equals higher reward. The problem with such a risk profile is that it is very similar to an investment in equities, where investors accept much less security for the upside of an ownership stake in the business. Higher risk (higher yield) bonds tend to be closely correlated with equities which means that such bonds do not really dampen volatility or smooth out returns over time when combined with equities in a portfolio. Both equities and high yield bonds tend to zig and zag, together. A sobering example of the downside this can foster was in 2008 when equities dropped 50% from peak to trough and high yield bonds also fell 40%.

{kind=link}

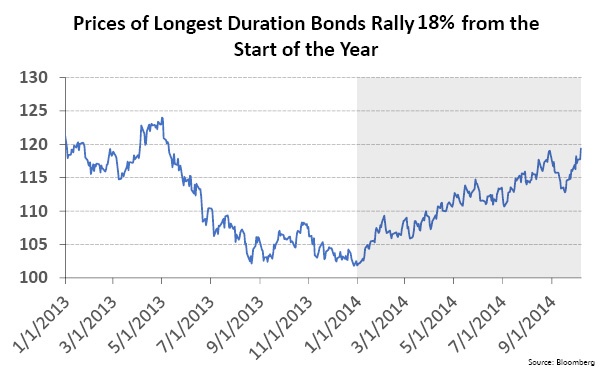

High Quality, Long Duration Bonds Perform Well When Times Get Tough

Can we improve upon this portfolio construction? Thankfully the answer is yes! With a little forethought we can use an underappreciated aspect of some bonds to provide welcome balance in the portfolio at those times when it is needed the most, in times of weak equity markets. Duration is the tool that makes this possible. Below we outline in more depth the underappreciated power and beauty of duration.

Duration is a simple concept: the length of time of the lending contract that the bond represents. The longer a bond’s duration, the more sensitive it is to growth expectations and inflation, both of which are falling now. The chart below illustrates this price appreciation in motion. Investors who had the foresight (What does the Bond Market Know, May 7, 2014) and Bond Market Clues, May 14, 2014) to buy long duration bonds have earned many years’ worth of returns in the last few months. US government bonds of 30 year duration have appreciated by 18% year to date. Holders of these bonds also locked in a coupon payment of 4% per year for the next 30 years should investors choose to hold these bonds to maturity. This return is more than twice that of more risky equities and more than three times higher than the return on high yield bonds this year.

The market earlier this year simply had made an enormous error by pricing in its expectations for a strong economic and inflationary environment that has frankly not appeared (Making Volatility our Friend: Trading the Kitchin Cycle, May 28, 2014 and Unsustainable Steel Premiums, Sept. 3, 2014). Those who recognized this error, and invested in long duration, high quality bonds have captured these outsized returns.

Isn’t it only natural that as growth and confidence fall investors naturally place a higher value on safety than they did when growth seemed more robust and confidence more well-grounded? Here we see one of the most powerful aspects of duration: its ability to act as a portfolio stabilizer, zigging when an equity heavy portfolio is zagging. Bonds of the highest credit quality and longest duration, US government 30 year bonds, have shown their power when an equity portfolio needed it the most. The clearest examples were their nearly 40% return in 2008 and again another 40% in 2011, periods of equity distress.

Everything is cyclical. We are confident that the day will come when the market fully embraces (and then some) our more controversial views on growth and inflation. The market will do so by increasing the price of the high quality, long duration bonds that we currently favor to levels that no longer offer a compelling return and margin of safety. At the same time, the market will be taking down the prices of higher yielding bonds as slowing growth leads investors to demand higher returns when taking credit risk. That will be the day when we gladly embrace credit risk in high yield bonds, when their prospective returns will be the highest – when investors are the most worried. This is the process by which we put our research to work using the levers of credit risk and duration to make money in the bond market and to stabilize returns over the cycle.•