Chief conclusion

Give each investment a fair and open-minded hearing, because the world is constantly changing.

Change Thrusts Investors into a New World, Creating Opportunity for the Open-Minded

Heraclitus is right that nothing endures but change. But how to identify change when it happens – and more importantly – how to profit from it as an investor? We believe that the disciplined application of logic and microeconomic principles, applied with an open mind, is one path to investing success. Cyclical volatility literally, used wisely, can be a never-ending source of potential new investment ideas.

There is always an industry in the market that is booming to amazing heights; just as there is always an industry in the market that is crashing to unbelievable depths. Volatility is constantly giving us new ideas on which to work, and new ways to make money in the markets. But while change creates the pre-conditions for profitable investment, investors must remain open-minded if they are to see and seize the opportunities that come from change. In today’s “Trends and Tail Risks” we explore rapid change in two industries, oil production and airlines, to see the challenges and rewards of recognizing, and profiting from, change.

A Case Study in Change: Oil Producers, Airlines, and Crude Oil

Oil production and airlines are two industries worthy of study because they show us how radically the world can change around an industry, and how profitable that change can be. This is not easy, as we explain below.

Imagine for instance, that its 2012 and you are an airline analyst. For the last fifteen years, you have been responsible for understanding the airline industry, what drives its fundamentals and how to make profitable investments in its stocks. You are smart, diligent, and hardworking. You are an expert on your companies and their management teams. There is only one problem – the industry for which you are responsible has been an unmitigated disaster.

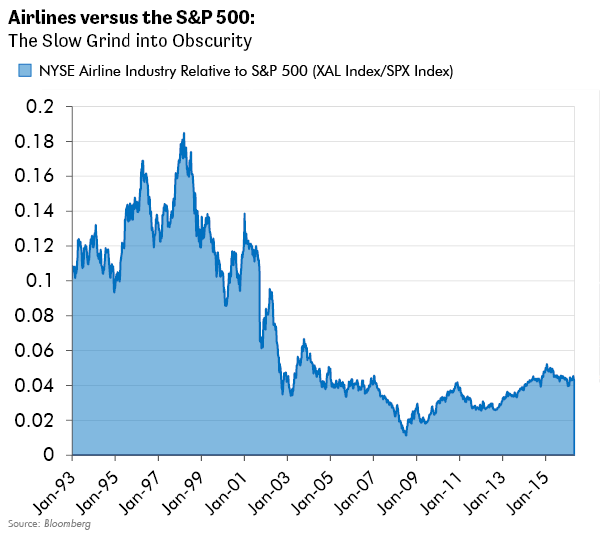

From 1998 to 2008, the airline industry underperformed the S&P 500 by 94%. The more than ten-fold rise in crude oil prices proved to be too much for airlines. After 2008, long-time leaders became insolvent and bankruptcies in your industry multiplied. Kicking you while you were down, Warren Buffett, told the world that only a fool would invest in your industry. Surely it seemed that your world was ending, not in a flash, but in a slow, grinding descent into obscurity. Night endured for so long that you began to doubt the Sun. Days turned into weeks, weeks into months, months into years, and years into a decade. There seemed to be no end.

In the later years of this underperformance, you were like the Maytag repairman: your phone never rang. You were undoubtedly an expert, but no one cared about the industry in which you had specialized. And why should they? After all, all your stocks ever did was go down. At cocktail parties, when people spoke of investments, lips curled in disgust once they heard you were talking about airlines.

It would only be natural if you got despondent and were the tiniest bit envious of the oil analyst: he had all the luck. You worked just as hard as he did. The only difference was luck: he was an expert in something that mattered. After all, crude oil had been rallying since 1998. In 2012, the prevailing topic of discussion that dominated the cocktail party scene would have been the U.S. energy renaissance. Think of it: U.S. energy independence! Trillions were invested in new energy production and distribution. It was a brave new world for that lucky energy analyst! He stood at the center of the investment universe. Life was good.

But this is not your world. You, the lowly airline analyst, have been laboring for years under an oppressive cloud of irrelevance and crushing disappointment. How objective could you really be after so long of a sustained beating? Even if you managed to find stocks that you liked during this period, how enthusiastic were you in promoting them? And even if you were, did anyone listen? Why bother? No one cares anyway. Your friends worried about you and tried to keep you away from sharp objects.

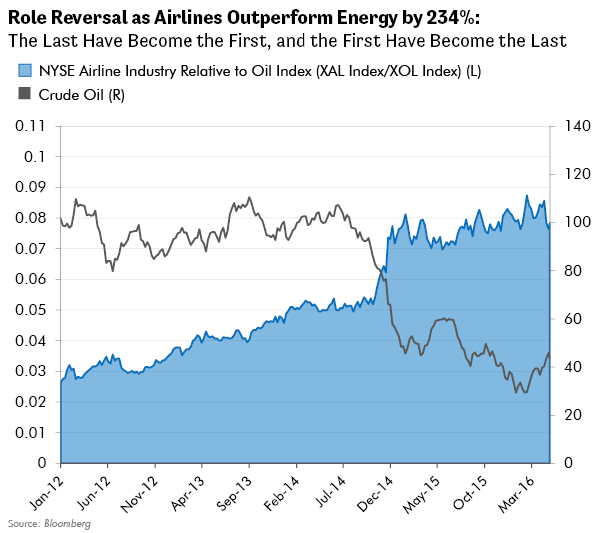

Into this miasma of suffering was born a run of performance that would be among the best in the entire stock market for the next few years. Airlines would strongly outperform the market, better yet, they would crush oil stocks by 234%, the very industry that was responsible for your industry’s underperformance. It’s that snooty oil analyst’s turn to suffer the indignity of presiding over his industry’s descent into the abyss. Now it is his industry becoming a byword for disaster and suffering. At cocktail parties, he is now the pariah. Anyone who bought one of his stocks had lost money. Karma’s blowback, though delayed, is powerful to behold. There is justice in the world.

Airline and Oil Investors Remember: This too Shall Pass

We think it ill-advised for any investor in either of these industries, or any industry for that matter, to become complacent. One could be excused for thinking that Lincoln directly cautioned investors when he noted that “And, this too, shall pass away.” If we have learned nothing else, surely we have learned that there is a time and place for everything. Each industry’s investment merits deserve a fair and honest hearing. A horrible past does not imply a horrible future; in fact, quite the opposite.

Valuation should dominate this discussion. Few industries contain equities that are durable enough to be “bought and forgot.” Most ride up and down on the waves of an industry’s cycle. Thankfully, our research can help us identify these companies, and when their industries are closer to the trough than to the peak. This is our goal. But the business of investing is humbling.

Four years ago few indeed would have forecast the amazing success enjoyed by the airline industry in the stock market. Two years ago, even fewer might have foreseen the collapse of the oil industry. Their fundamentals changed dramatically and quickly. What will the future hold for each industry? If we had to bet, our confident prediction would be for change.

Common Principles Across Industries: Lessons from Oil Producers and Airlines

Karma notwithstanding, we would argue that a few causal factors lay at the root of the reversal of fortunes in these two industries. These help to explain why it can be hard for “experts” in their respective silos to spot change in their own industries. This lies at the core of our belief that those who specialize in change itself can create their own sustainable competitive advantage. Once the principles of change have been mastered, these techniques can be applied to industry after industry as the market serves up a never-ending diet of change.

One factor that conspires against the overly-specialized “expert” in his silo, is the fallacy of trend extrapolation, the understandable but flawed belief that tomorrow will look like today. The majority of time this will be true. The problem is the minority of times when the world changes. Often those closest to an industry can be the last to see that kind of change. Because trend changes can be rare and long-deferred, few can remain vigilant.

For instance, it would only be natural for airline experts to look upon the widespread bankruptcy that engulfed the industry as a sign of failure, of the culmination of a long period of financial distress. When we looked at the group, however, with fresh eyes in 2012, we could draw upon past periods of cyclical distress in other industries and draw a more hopeful conclusion. We had experienced, and profited from, periods of bankruptcy in industries such as fertilizers in 2002, when 25% of the industry was in bankruptcy, and steel in 2003, when more than 40% of capacity was in bankruptcy.

As global investors scouring the world for such industrial distress, we had seen before in these examples how, post-bankruptcy, new management teams and fewer competitors had led to more disciplined capital spending and the rationalization of capacity. Furthermore, consolidation can put a floor under asset values, as entrenched competitors look to take out weaker players. This gives investors multiple ways to win, even if a turn in the cycle ends up being delayed.

Post disaster, the recent history of capital destruction makes everyone – company management teams and investors alike – leery of overinvesting. Ebullient CEOs who confidently and wrongly over-expanded have been discredited and fired. New CEOs get the message: be smarter and more disciplined. Don’t overspend. Cut costs. Reduce debts. This is the rise of the bean-counters. Where once the risk-taking, gun-slinging cowboys reigned, now all that can be seen are accountants, hired to stabilize the mess they inherited. The dangers of leverage are on everyone’s mind, so a large part of any available capital goes into reducing debts, not expanding capacity. Even the credit market seems to conspire against the industry by cutting off the flow of funds that once readily enabled over-investment in the industry.

Lather. Rinse. Repeat. The Cycle Never Changes

Of course, eventually, the bean-counters and their newfound conservatism gradually leads to under-investment in the industry. Demand growth begins to outpace stunted supply growth, and a tightening supply/demand balance leads to rising prices and better economics. Returns on capital start to rise. The industry’s recovery seems miraculous. Its many long disappointments are forgotten. Sadly, investors have almost no memory. In time, all its former errors will be repeated. But not yet!

The new crop of “visionaries” among the companies’ management, were those who earlier pushed for capacity expansion or aggressive purchase of competitors. Events have now proven them right. The newly discredited bean-counters get fired because their overly conservative management has left their companies behind in the chase for growth. The visionaries, who once long ago were called by another name, cowboys, are on the rise. Better economics in the industry drive a falling cost of capital, even the credit markets now conspire against discipline. No Texas-sized expansion plan is too aggressive, no matter how hair-brained. All projects, even the highest cost ones, get willingly and unquestionably funded by permissive credit markets, from which, seemingly all memories of past disasters have vanished. Caution will not be the prevailing emotion but rather jealousy of the lush returns made earlier in the cycle by prior investors. Confidence and complacency reign. What could possibly go wrong in this, the best of all possible worlds?

In Conclusion: Our Core Principles are the Same Regardless of the Industry or the Cycle

Change is inevitable. Almost every industry trend will at some point reverse. Those industries earning high returns will see those returns decline and those industries making poor returns will likely recover. We spend most of our time looking for sectors where returns have been poor to identify when the inevitable trend change will reverse. Often our interest in such sectors seems controversial.

However, we must be thoughtful investors. We look for the lowest cost producers with the best balance sheets. These companies tend to have the best management teams. If they are supported by good valuation, usually measured by a substantial discount to replacement cost, and further under-pinned by the positive carry of a defensible dividend stream, we are ready to invest.

After we invest, over time, we must remain vigilant for change. The volatility that drives the cycle never ends. Any industry, if successful enough, can become overly exuberant. Success often brings with it expanded valuations, which are definitely welcome, but carry growing downside risks to our investments. So we buy early and sell early. Over time, the industries in which we invest change. What does not change is our investing methodology or the discipline with which we apply it. •