Chief Conclusion

We noted two weeks ago that our trusted indicators in the steel markets had signaled that the inventory cycle was turning lower. We expect higher-quality, longer-dated bonds to outperform and growth sensitive commodities and financials to underperform as markets deal with the shock of slowing economic data “out of nowhere.” The Financial Punditry may seek to lay the blame on “turmoil in the White House,” but this is simply the inventory destocking cycle arriving on time and on schedule.

Our goal in writing “Trends and Tail Risks” is to help our readers understand the principles and thinking that drive our investment decisions. Our research makes us different and is a big part of the value we seek to add to client portfolios.

Two of our most important and foundational principles are 1) understanding cycles and 2) thoughtful asset allocation - owning the right assets at the right time. We try to use every tool and trick we have learned during our nearly twenty years in the markets. One of the tools that has served us well has been understanding the inventory cycle, earned from our extensive study of the steel markets.

Two weeks ago we wrote “Preparing for a Peak in the Inventory Cycle” which noted that our trusted indicators were flashing a warning that a deceleration was upon us in this trillion dollar market. We noted that inventory destocking cycles were global events that expressed themselves in rising prices for the highest quality, longest duration bonds (falling yields), and in worsening credit quality. We will not repeat our analysis here but would suggest readers refer to our research on this topic for more background (“Making Volatility Our Friend: Trading the Kitchin Cycle, Unsustainable Steel Premiums, and Revisiting the Inventory Cycle).

Since then, the equity market as a whole has largely ignored - until today that is - the signs of distress we have flagged in steel that are spreading to other markets. A few of these have been particularly noteworthy, such as the dramatic weakness of the Chinese stock exchange, Chinese iron ore and steel prices, and the meltdown at Home Capital (HCG CN), Canada’s largest subprime mortgage lender. We are also watching the premium that the market demands to fund riskier debts rise - from a very low base - here in the U.S. While many seek to dismiss these events as “isolated,” our study of cycles shows that often the dots connect when there is a change in the cycle. We believe this is occurring now and that the market is mispricing a variety of assets.

Automotive Markets: Next Shoe to Drop?

A key leading indicator of future automotive production cuts may be found in the steel market. Let me explain.

When weakness in auto sales leads to automotive production cuts, automotive producers relay this information to their steel suppliers. These suppliers, chiefly U.S. based integrated steel producers, suddenly find themselves the unhappy owners of excess steel; steel that they had thought was already sold. Many of these companies dispose of this newly redundant supply ignominiously in the spot steel market, which is not a natural home for their products. When this happens, savvy observers begin to expect automotive production cuts.

I remember very well how this chain of events flowed during the inventory destocking cycle of 2005. In February of 2005, major integrated steel producers showed up “out of nowhere” dropping tons into the spot market. Many explained away, for various reasons, this development. The truth came out, however, on April 15 when General Motors announced cuts to its production schedule. The next six weeks witnessed some of the most violent trading I had ever seen. Our research indicates that once again integrated steel producers are selling tons in the spot market. Will past be prologue? We think the answer is yes.

Identifying the Weak Links in the Credit Chain

The chain of credit that binds the global economy together always breaks at its weakest link. The weakness unfolding in these markets has our full attention, because as they weaken, they identify themselves - potentially - as the locus of the next credit-driven downcycle. Our best investment results historically have followed the correct and early identification of problem areas. Big trends start small.

What are the first steps investors should take to protect their portfolios from an unexpected slowdown? Our belief is that the ownership of higher quality, longer duration bonds, can be one of the best tools to weather this volatility, as we outline below.

Investors Do Not Understand Bonds. Here Is What They Are Missing.

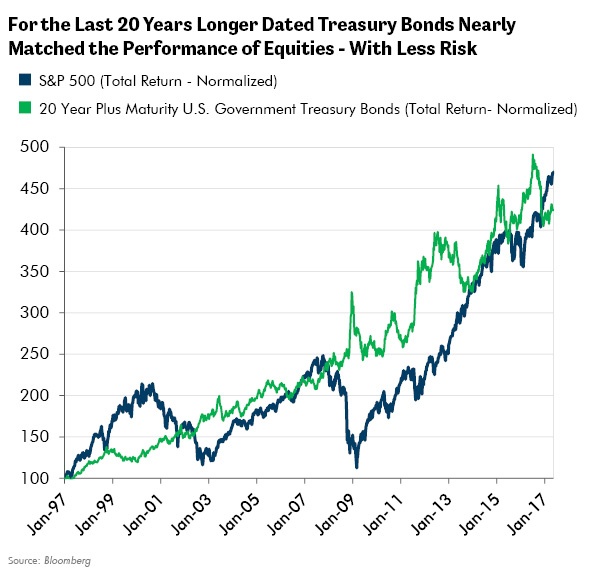

As the chart below displays, bonds over the last twenty years have provided an excellent return, nearly matching that of the S&P 500.

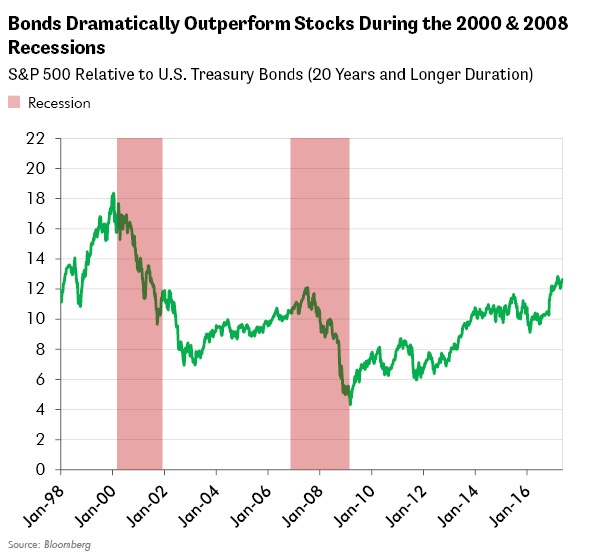

The ownership of higher quality, longer dated bonds has been particularly useful in mitigating downside risk in equities from the peak of economic activity to the trough, such as from 2000 to 2003 and from 2007 to 2009. The chart below shows the ratio of the S&P 500’s total return divided by the total return of U.S. government bonds with a duration of twenty years or longer. When the line is rising, equities are outperforming bonds. When the line is falling, bonds are outperforming equities. The colored areas outline recessions.

In fact, the total return of the S&P 500 underperformed the return of bonds by 62% in the 2000 recession and by 64% in the 2008 recession. We believe this data supports our long-held view that these bonds provide diversification to equity-heavy portfolios. This protection is particularly welcome during times of decelerating economic fundamentals, such as the current inventory destocking cycle now underway.

No one can tell for sure whether the slowdown now underway is a temporary “air-pocket” or the start of something more sinister. One thing is clear, however: bonds will prove their merit either way.

The Miracle of Higher Quality, Longer Dated Bonds

Through many hard fought campaigns we have built our investment philosophy. One of the most dearly purchased of all those lessons is this: there is more money to be made being long the solution than short the problem. The ownership of higher quality, longer dated bonds is the most elegant solution to slowing economic data for this and many other reasons which we outline below.

First, these bonds have a negative beta to the S&P 500 - negative .4 to be exact for the U.S. government 30 year bond. This means that typically they tend to rise in price by 0.4% when equities fall in price by 1.0%. Second, these bonds combine this handy trait with positive carry, which is a fancy way of saying that they pay you while you wait. This allows investors to be “early” and not sacrifice returns. Contrast that with the negative carry of owning put options or shorting stocks with dividends as hedges! Bonds are a much more forgiving investment when it comes to hedging an equity portfolio. Third, these sovereign bonds have almost no counterparty risk, nor liquidity risk, nor hidden fees, nor complex structures. If ever there was a useful hedge for today’s environment, it is such bonds.

In Conclusion

You might think that such an elegant and uniquely powerful construction as the bond would earn the universal respect of market participants. But there you would be wrong. Instead, the bond is scorned universally by a dedicated cadre of vocal market participants who willfully blind themselves - and anyone who will heed them - to its many merits. Frankly, this is just fine with me.

Our clients pay us to understand the difference between hype and substance and to worry for them, avoiding the pitfalls our research may identify before they become problems. Our study of the steel markets, and of cycles, are just a few of the ways we put our research into action for our clients. We believe our higher quality, longer dated bonds will prove their merit, once again, as valuable holdings in a slowing economy.•