Chief Conclusion

We have watched and waited for a decade for Potash Corp. of Saskatchewan (POT) to become cheap enough to purchase again. A few days ago, we finally pulled the trigger and decided to invest. Below we outline how our unique analysis helps us to identify value and how we are continuing to find compelling investment ideas despite new all-time highs in many markets.

Our clients may have noticed a recent addition to their portfolios, POT. This is not an investment in cannabis, rather the stock of the world’s largest fertilizer equity, Potash Corporation of Saskatchewan. The company is a low cost producer in the much-beleaguered fertilizer industry. Fundamentals there have collapsed from unbelievable highs to stressful lows. This competitive pressure is driving consolidation and management changes throughout the industry, which are encouraging signs that better days may lie ahead. Today’s “Trends and Tail Risks” outlines what we think are Potash Corp’s investment merits.

To Find Value Where Others Don’t: Look Where Others Don’t

More than a year ago, we asked the question "is this the bottom of the agriculture cycle?." We outlined then that we were seeing a number of signs that we have witnessed many times before at meaningful lows in deeply depressed industries. Our analytical team has spent almost its entire collective career specializing in change and in industrial distress, which means we have traded well over a hundred different cycles globally, in many industries. While their names may be different, the pattern and our investment process remain the same.

In our near twenty years of investment experience, one of the best signs of a real low, is the bankruptcy of weak and overly-leveraged producers and consolidation among competitors. Why? This removes excess supply – which was formerly weighing upon prices – and lowers the cost of production for the remaining producers. These are rational actions for companies in times of cyclical distress. They are the leading indicator of future financial improvement. For that reason, the announced merger between fertilizer producers Potash Corp (POT) and Agrium (AGU) caught our attention more than a year ago.

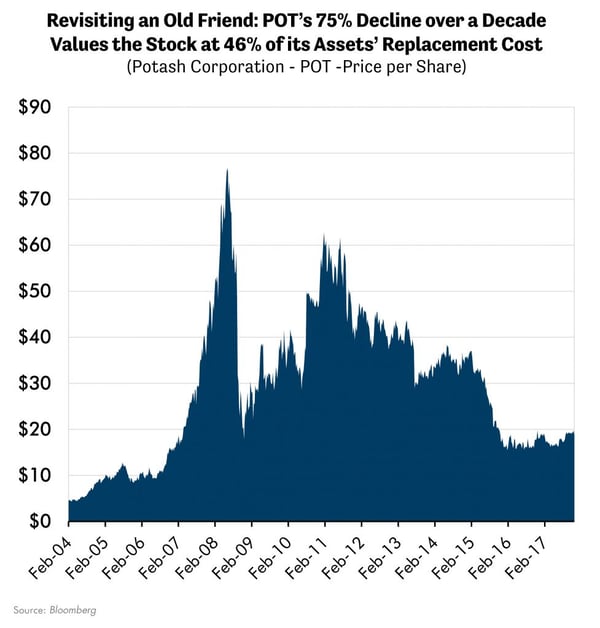

So we updated our valuation analysis. And waited. Real, sustainable bottoms take a long time to form. My good friend of many years and a well-known technical analyst, the ever-insightful John Roque, once told me that “Bottoms are a process and not an event.” How right he was. These things take time. We think the chart below suggests that POT’s 75% decline over the last decade has the stock very far along in its bottoming process.

Finding Value Where Others Don’t: Valuing Companies Differently

One of our best tools to see what is not obvious, and to discern value that others have overlooked, is the valuation methodology of replacement cost. Replacement cost is a simple idea. Think of a company as a bag of assets. Replacement cost valuation asks: what is the value of the assets in the bag? We seek to buy the bag (the stock) when it trades at a deep discount to the value of the assets in the bag. Simple right? After all these years, I am still amazed that so few do this.

We first outlined this valuation methodology in June of 2014 and would refer you to it to learn more.

Our updated valuation suggests that POT is trading at less than 50% of the costs to replace its assets. Or, thought of another way, if you wanted to enter the fertilizer business, we believe it would be 50% cheaper for you to do so by buying POT stock in the open market rather than by writing a check to build the assets yourself. A big part of this dramatic undervaluation comes from an underappreciated part of the company, its investment in other public companies.

POT owns nearly $6 billion in equities of other publicly traded companies. The largest of these is in Chile’s SQM, a potash and lithium producer whose stock has appreciated more than 100% this year. These investments represent more than 1/3 of POT’s equity value. I expect the vast majority of these holdings to be sold and converted to cash in the coming months as required by the global regulatory bodies who have required this step in order to approve the merger of POT and AGU.

While the ultimate disposition of this future multi-billion dollar cash hoard will be up to the board of the newly combined POT and AGU, my fifteen years of experience with POT’s savvy chief financial officer (CFO) Wayne Brownlee gives me confidence that the company’s culture is to apply capital to the best benefit of shareholders. Over the long years that I have known Wayne, beginning in 2002 when T. Rowe Price purchased 8% of POT, Wayne has proven to be one of the most disciplined and thoughtful CFOs with whom I have had the pleasure of working. The company’s incoming board is lucky to have access to his counsel.

In Conclusion: We Continue to Find Value Despite New All Time Highs in the Stock Market

Despite the fact that markets seem to hit new all-time highs every day, we continue to find undervalued investments. For instance, our analysis of POT suggests that the stock presents us with a 6x1 ratio of upside to downside. Put another way, for every $1/share we risk in loss if we are totally wrong, we stand to potentially gain $6 if we are right. Now those are odds that merit our investment!

To calculate these numbers, we assume that we have no insight into the future, that we have an equal chance (50/50) of being wrong as we do being right. We derive our estimates of downside and upside from our long history with replacement cost analysis, which assumes downside to 40% of replacement cost and an upside to 100% of replacement cost. I hope you can see how replacement cost valuation is one of our most powerful secret weapons.

Six to one is truly a compelling ratio of reward to risk. We believe many investors miss these opportunities because of their desire for more “near term visibility.” While understandable, such investors are giving up protection that they could have against an uncertain future: an attractive price at which to begin their investment. This is why, when we speak to you in these letters, we always hammer home the importance of patience. If this were easy, everybody would be doing it. Many investors are not and this gives us our opportunity! •