Chief Conclusion

Rising political risks combined with worsening credit quality and central bank tightening are among the most important themes for investors to consider when making capital allocation decisions because they speak to where we are in the current market cycle. With this backdrop, our work suggests that gold related investments and the highest quality bonds, will return to their historical position providing diversification benefit to an equity portfolio as we approach the end of this cycle. For proof, however, we will have to wait to see what unprecedented central bank asset sales will do to prices and to financial volatility.

If there is anything I have learned in nearly 20 years of professional investing, it’s how fast the market can change. Why is that? Because human emotion, a fragile flower, is what ultimately drives markets day to day. Human nature and human emotions have not progressed in thousands of years. Thus we can better understand today’s markets by studying historic markets.

I try to study the precedents that best match our current environment, and how it may change. For about the last year and a half I find myself drawn to the study of the last days of the Roman Republic, when the old order was ending, and a new order was beginning. It was defined by a collapse in trust in the Republic’s institutions, a divisive gap between have and have-nots, the rise of political violence and a corrosive growth in tribalism – where right and wrong mattered less than supporting the leader of your tribe. Sound familiar?

As political uncertainty reached a fever pitch, long-term planning collapsed under the pressure. People stopped investing and – during the most acute phases of crisis – even took to burying their wealth! Burying your wealth is the ultimate sign of the loss of confidence.

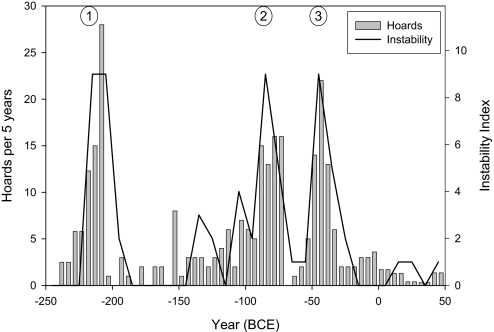

When the Going Gets Tough, The Tough Start Digging

The chart below from Peter Turchin outlines three peaks in coin hoarding during the final years of the Roman Republic. The three sharp peaks in columns show 1.) Hannibal’s invasion of Rome, 2.) the Social and Civil War of Marius Vs. Sulla, and 3.) the Roman Civil War that started between Pompey and Caesar, whose conclusion ended the Republic.

The solid line represents political instability. The correlation is clear: at high enough levels of political instability, confidence can collapse driving people to bury their hoard of coins, the money of the day. Falling confidence also expressed itself in falling prices and commercial activity, such as Cicero complains about in his letters to Atticus (see opening quotes above).

Source: http://www.pnas.org/content/106/41/17276

Source: http://www.pnas.org/content/106/41/17276

In today’s “Trends and Tail Risks” I wanted to explore the prospects for rising financial volatility especially as central bank asset buying turns to selling.

Global Populism: The Rise of the New and Uncertain Order

Unless you have been in a cave for the last few years, you will have no doubt noticed that the world’s existing political order is fraying. The Global Financial Crisis, European sovereign debt crisis, Brexit, and the global rise of populism suggest that the post-World War II system is ending. That order was defined by the norms of 1.) free trade, 2.) international cooperation, 3.) a U.S. security umbrella for much of the world, and 4.) the integration of Europe. These are huge changes. One major implication is that long term planning is getting a lot harder for businesses with global interests.

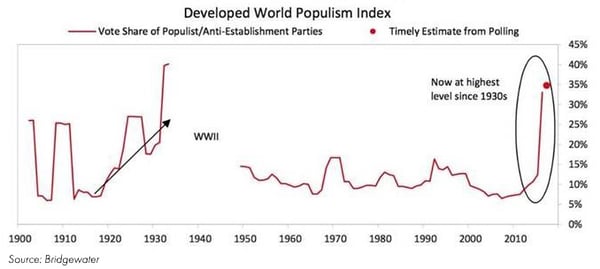

The chart below from Bridgewater, the world’s largest hedge fund, shows global populism at the highest levels since the 1930s.

Something’s Gotta Give: Rising Political Uncertainty and All-Time Low Financial Market Volatility

One of the most puzzling things in the market is the startling dichotomy between rising political uncertainty and – until very recently – all time low financial uncertainty. We wrote about this more than a year ago asking, “Is Low Volatility Sustainable with Populists in Power?”

We can measure financial uncertainty through the VIX, which is an index that measures future expectations about the volatility of equities, the junior tranche in corporate capital structure. Only six weeks ago the VIX hit the lowest level ever recorded. How to explain this dichotomy between low financial volatility and sky-high political volatility? We think the answer is unprecedented central bank asset purchases, which goes by the name of “quantitative easing.”

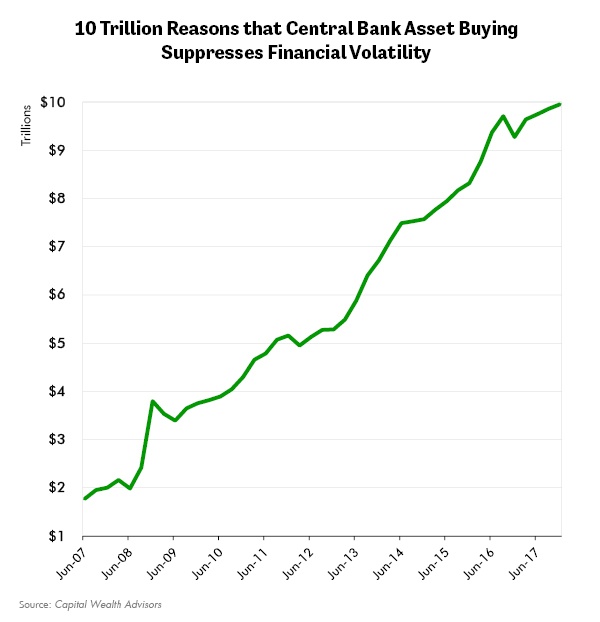

Financial Volatility Suppression 101: Central Banks Create Money from Nothing to buy Ten Trillion Dollars of Assets

It’s a reasonable hypothesis that the ten trillion dollars spent by the world’s central banks to buy assets has helped to suppress financial volatility in the face of rising political volatility. In fact, I would suggest that central bank buying exploded because political volatility rose, as I will explain later. The chart below shows the relentless Central Bank buying. How much did this keep political uncertainty from becoming financial uncertainty? No one can say for sure, but I am willing to guess a lot.

The numbers are so big that they are difficult to understand. Just one example: the Swiss National Bank owns more Facebook than Mark Zuckerberg, the company’s founder. This is real money. I think it’s having a real impact, as the example below explains.

Mario Draghi, the head of the European Central Bank (ECB) gave a speech on July 26, 2012 where he promised to “do whatever it takes.” It shows the power of central bank asset buying. Below I quote from his comments:

“Then there’s another dimension to this that has to do with the premia that are being charged on sovereign states borrowings. These premia must do, as I said, with default, with liquidity, but they also have to do more and more with convertibility, with the risk of convertibility [e.g. a country now using the Euro makes the political choice to leave the Euro and issue its own new national currency. Emphasis mine]. Now to the extent that these premia do not have to do with factors inherent to my counterparty - they come into our mandate [emphasis mine].”

European sovereign debt markets were in turmoil as investors priced into the markets their fear that the Euro currency experiment could end in failure. The greatest risk was that large debtors such as Italy and Greece would take the political step of leaving the Euro to adopt new currencies, so they could devalue and have their central banks print the money to “fix” their problems. This was the “convertibility” risk that Draghi outlined. These fears drove losses in the market prices of bonds in Italy, Greece and other troubled European countries. As bond prices fell, interest rates rose, stifling growth and thus creating the outcome that so terrified the markets.

Draghi’s speech literally turned the markets on a dime. The most troubled bond markets in Europe began to strengthen on the promise of unlimited central bank asset buying by the ECB. Note that markets were suffering from political risks. Political risks have gotten worse since then and now central banks plan to reduce asset purchases? Am I the only one that thinks this could cause trouble?

Will Financial Volatility Rise to Match Political Volatility as $10 Trillion of Central Bank Buying Turns into Selling?

Central bankers have announced plans to turn their asset purchasing programs into asset selling programs over the next few years. I think investors are underestimating how much financial volatility will be unleashed as this unprecedented volatility suppression unwinds.

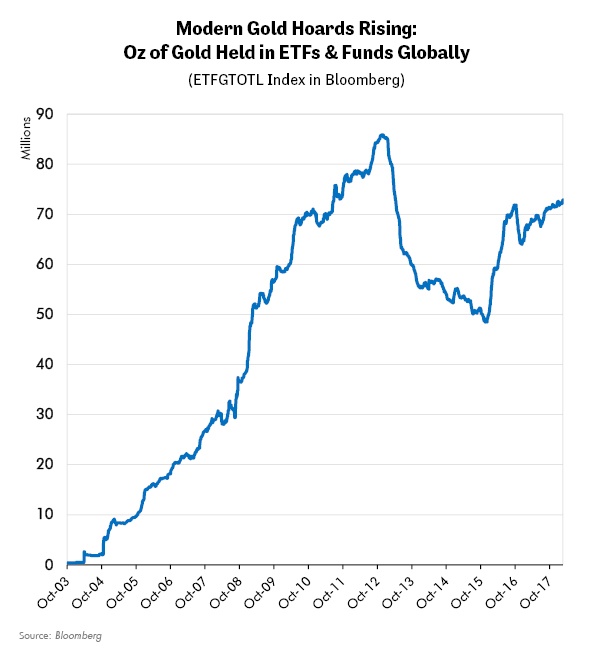

Modern Day Wealth Burying: Watch the Daily Quest for Safety in the Ounces of Gold Held in the World’s Gold Funds

The same fear that gnawed on Romans, driving them to hoard their coins and seek safety two thousand years ago is alive and well today. We can measure this level of fear every day on Bloomberg in the number of ounces of gold held in the world’s gold exchange traded funds (ETF). This gives us a profoundly insightful tool to measure in real time the level of concern in the markets.

The chart below illustrates how this proxy for investors’ fears peaked right after Draghi’s speech and fell dramatically for three years as Draghi’s ECB joined the quantitative easing fray to buy time for the European political status quo and the Euro. Interestingly, gold held in these vehicles began to rise again in 2015 as the trend of global populism strengthened with elections in Europe, Brexit, and eventually the Trump Administration rapidly advancing the populist cause. Is this the sign of things to come? As central banks wind down their asset buying programs, I think we will see the truth clearly.

Conclusion

Timeless human nature is still driving our markets two thousand years after the fall of the Roman Republic. Thankfully, modern indicators, such as the one above, can help us gauge where we are in the never-ending human cycle of fear and greed. It’s noteworthy that despite near all-time highs in most asset classes, some stubborn fear continues to drive gold ownership higher. I expect this to accelerate as central banks begin to sell assets and thus expose the financial markets to the same high level of volatility we see now in the political world. Also, once the credit cycle begins to turn down from elevated levels this trend should accelerate. We discussed our current thinking on the credit cycle recently in Feed the Ducks While They Are Quacking.

The new trends of worsening credit quality and central bank asset sales are important for investors because they speak to the most appropriate asset allocation for where we are in this market cycle and the world’s rising political risks. Our work suggests that gold related investments and the highest quality bonds, despite recent weakness, will demonstrate their historic diversification benefit to an equity portfolio when this current extended cycle ends. For proof, however, we will have to wait to see what unprecedented central bank asset sales will do to prices and to financial volatility. The challenge of investing is that we must make decisions now about how to navigate the challenges we will face in an uncertain future. Our investors pay us to study these issues deeply such that we can have an informed view ahead of the news. These pages outline our current thinking and why we hold those views. Please contact us if you would like to discuss this further. •