CHIEF CONCLUSION

Our investment framework has gold as the leading indicator and driver of higher commodities. In today’s “Trends and Tail Risks” we outline why we believe that this is bullish for all commodities, and furthermore, why we see a compelling opportunity right now in the corn market. Finally, we outline why we think that the corn market – the biggest in agriculture – is in a new bull market and what that means for other markets as well. We believe that events underway create a rich new idea set for our research team to analyze.

You see, there is only one constant, one universal, it is the only real truth: causality. Action. Reaction. Cause and effect. - Merovingian in "Matrix Reloaded"

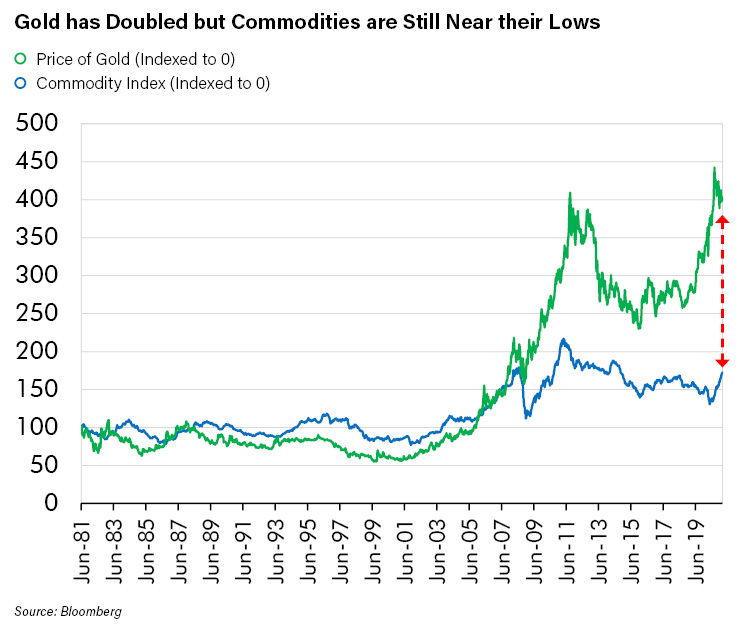

Gold: why the Gold Price Matters for Commodities

One key theme that has characterized our recent investments, and should continue to do so, is a broadening of our investments from gold – which leads the commodity complex - into other commodities and real assets. Our thinking is that, with a doubling in the gold price in the last five years, we should see upward price pressure on all commodities. Before we do a deeper dive on one commodity – corn – about which we are very bullish, we thought it would make sense to quickly recap our thinking about why gold leads commodities.

We have concluded, after decades of study, that the strongest commodity rallies begin with gold, because gold reflects the fluctuating value of the dollar and in fact all currencies. Here, we mean that as the gold price goes up, it is really a reflection of currency values going down. For instance, if gold doubles in dollars, its really a reflection that – in gold terms – the dollar’s value has been halved – put another way, that it takes twice as many dollars to buy the same amount of gold. This has major investment implications, as we discuss below, for commodities.

When the value of the dollar drops, it means that the cost to make many things – especially commodities – will face upward price pressure. Remember what you learned in your Microeconomics 101 class in college: that in the long run, commodity prices converge to their marginal cost of production. So, if commodities marginal cost has doubled, because the gold price doubled (and the dollar’s value halved) then it makes sense to analyze the commodity complex to identify the most compelling ones. Ones that have other intrinsic factors that make them the most compelling to own against a backdrop of generally rising prices. In today’s “Trends and Tail Risks,” we do that deep dive on corn, where we think that the stars are aligning for a very profitable investment campaign.

The Bull Case for Corn Starts in China

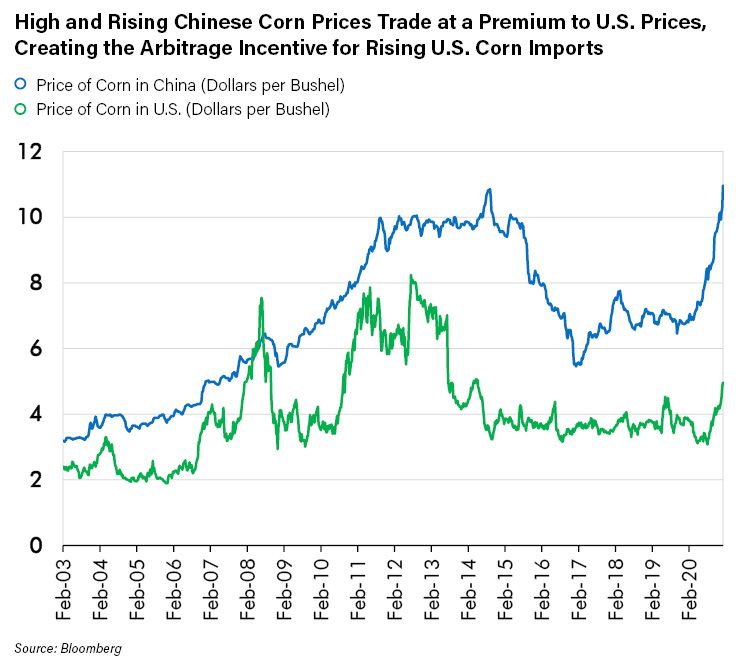

Below is the price of corn in China shown in US dollars per bushel. Two things are readily apparent. First, it is at a new all-time high. Second, it has nearly doubled in the last 18 months.

For the Chinese Communist Party, which has enjoyed one party rule in China since 1949, this is very bad news indeed. The fastest way to de-legitimize Chinese Communist one-party rule is to allow inflation to take hold, particularly food inflation, which can be very painful to the hundreds of millions of poorer Chinese for whom food affordability is a serious issue. Increases in food costs have often led to social unrest. Though some may have forgotten that the Tiananmen Square protests followed meaningful food inflation in China in 1988, the Chinese Communist party leadership probably has not.

The main use of corn in China is for animal feed, particularly for pork. Pork production is very corn intensive, meaning that on average it takes three pounds of corn feed to create one pound of finished pork. Furthermore, the price of pork itself has already doubled in the last 18 months, which is both highly destabilizing and is likely focusing the mind of China’s Communist Party rulers in a powerful way. As you would likely imagine, an analysis of the potential for higher U.S. corn prices – and an improving U.S. farm economy – also starts in China. Below, we show a chart illustrating how Chinese corn prices compare with those in the U.S.

High and Rising Chinese Corn Prices are Dragging U.S. Prices Higher

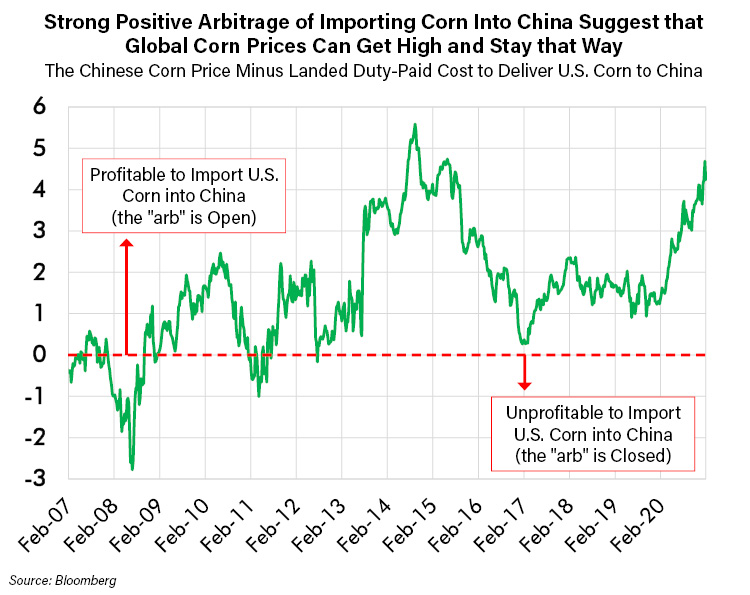

Chinese corn prices are twice those in the United States. This is providing a powerful incentive for China to import a lot of lower priced U.S. corn. For China, the fastest way to address a spiking corn price is to import corn. A lot of it. That is exactly what China should start to do – right now - in a very meaningful way, with very bullish implications for the world corn market. In fact, the chart below shows the “arb” or profitable arbitrage potential that now exists for traders to make a lot of money shipping U.S. corn into China.

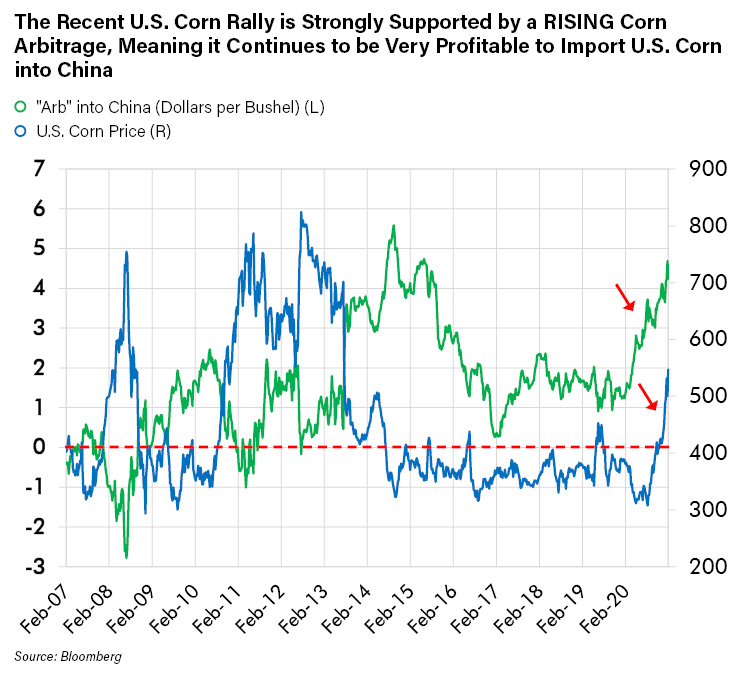

The Recent U.S. Corn Rally is strongly Supported by a RISING Corn Arb, meaning it continues to be very profitable to import US corn into China

We calculate such arbs because they are one of the most powerful ways to predict how the market will use prices to allocate resources. According to my calculations represented in the example below, traders can pay all the cost of buying U.S. corn, shipping it from where corn is harvested to U.S. ports and then overseas to China and still put several dollars per bushel of pure profit in their pocket. This extraordinary profit potential is how the market balances supply and demand. In this case the market does so by incenting the import of millions of tons of U.S. corn into China through the “invisible hand” of the above arbitrage opportunity or profit motive. As we have said many times, price allocates resources.

That is only the beginning of China’s bullish impact on the global corn market. According to USDA estimates, believed to be the most accurate of those publicly available, China accounts for 2/3 of world’s inventories of corn. However, the twenty years I have been following the corn markets have convinced me that there is substantial uncertainty in quantifying China’s corn inventories with any confidence. So, I have come to distrust any estimate of China’s inventory numbers, even those from the USDA. I do, however, trust Chinese prices. Chinese prices are on the move now in a big way. In fact, they are screaming that the country is desperately seeking much higher corn imports. Perhaps Chinese corn inventories are lower than many think? If so, it has deeply bullish implications as we explain below.

We can, however, have much stronger conviction in corn inventories outside of China, particularly those in the U.S., the world’s chief granary. In fact, the U.S. represents fully one half of all the corn inventories outside of China – so prominently does the U.S. figure in the global corn markets. Those inventories are dropping – and are projected to drop even more. In the most recent USDA report (January’s WASDE report), estimated U.S. corn inventories are projected to drop from an earlier estimate of 43.2 million metric tons down to 39.4 million tons. Estimates of imports into China rose to 17.5 million tons and could and should go a lot higher especially with soybean imports five times that at nearly 100 million tons. China has poor factor endowments when it comes to making corn. In fact, China is a high-cost producer with weak soils, bad genetics, and yields that are much inferior to our own. If China were to import something closer to 100 million metric tons of corn, it is not clear where that corn would come from. Of course, U.S. farmers – as the world’s low-cost producers - would be dramatic beneficiaries. That is where our potential corn-related investments come in.

There are Many Ways to Profit from Higher U.S. Corn Prices

Higher corn prices improve the prospects of many agriculture related businesses. For instance, higher corn prices and improved economics for U.S. farmers create the incentive to re-invest in their business through 1.) new farm investment such as tractors or irrigation equipment, or to boost farm production through 2.) more intense usage of fertilizers, or 3.) higher yielding seed varieties or greater pesticide/herbicide usage to maximize income at higher corn prices. In each of these sectors, there are a handful of great companies globally with which we are familiar. These are companies we have known and studied for years. We have just needed a reason to think that their fundamentals were ripe for sustainable improvement. We believe that the changes underway in the corn price now give us that reason. We intend to invest accordingly!

A Very Inter-Connected World! Other Implications of Higher Corn Prices…

We believe that there are also many more subtle and indirect ways potentially to profit from our research team’s insight into the corn market. For instance, corn is the dominant agricultural commodity in the U.S. Our country planted 92 million corn acres in 2020 versus 84 million soybean acres, 44 million wheat acres, and only 12 million cotton acres. Because there is only so much profitable farmland that can be planted, farmers will shift more of their land to the most profitable crop they can grow. This means, naturally, that farmers who can plant more corn may – in the short run at least – plant less of commodities whose prices are lagging.

This underscores the first investment implication of higher corn prices: less U.S. supply of wheat, soybean and cotton and therefore likely upward pressure on their prices. And because each of these commodities has an impact on a global supply chain, we potentially have many ways to thoughtfully invest in each instance. For example, higher cotton prices can work to reduce demand for higher priced cotton and create more demand for products that are lower priced substitutes for cotton fibers, such as rayon fiber. There are a handful of companies globally that make rayon, that we have been researching and following for years. We doubt that many other investors understand the hidden impetus higher corn prices can provide to this small corner of the global market. So, we believe that this is just one example of how a higher corn price can create an investment opportunity for those that understand these markets.

In Conclusion

I hope now that you can see why our research team loves change. As the corn market has rallied, responding to the growing import arb into China, a whole new world of potential investments has opened before us. Many new potential investments, companies we have followed for years, just became much more interesting to us. Before they may have been just cheap – but they were going nowhere. Now they are cheap – and improving! Improving for reasons we understand and in which we can have confidence. What a difference that makes to our process! Its another great example of our long-held belief that there is truly always a bull market somewhere – if you know where to look that is! Certainly, we believe that a new bull market is underway now in corn. We intend to invest accordingly.