CHIEF CONCLUSION

The U.S. Federal Reserve met this week to consider its interest rate policies. The market seems to be increasingly pricing in that a too-slow Fed is falling further behind the curve, especially with the warning of an inverted yield curve. If so, we believe the odds are growing that the Fed may have to dramatically increase the pace of its future interest rate cuts. Accordingly, it is our belief that the mortgage REIT sector may now be suffering its period of maximum uncertainty, which has historically resolved to the benefit of shareholders once it’s clear that the Fed is on an aggressive path to cut interest rates.

Our investing is valuation-driven, not sentiment driven. So, in our investments we actively seek out companies that we believe are undervalued and may face great uncertainty. Often these investments have already been poor performers. Sometimes that continues even after we get involved. This typically means, however, that we like these ideas even more. Why? We already thought they were cheap. Now, they are cheaper, in our opinion. We like to buy things that are down because that is often where the value is! We believe that opportunistic, global investors can always find smart risks to take, and that today’s problems can become tomorrow’s solutions for those with patience and discipline.

“It is only the farmer who faithfully plants seed in the Spring, who reaps a harvest in the Autumn.” – B.C. Forbes

The U.S. Federal Reserve met this week to consider its stance on interest rates, namely whether to cut interest rates again, by how much, and to indicate its intended future policy. The market had already spoken about what it expected. The futures market (WIRP Function in Bloomberg) showed that the market was pricing in a 100% probability of a Federal Reserve interest rate cut of some magnitude, either 25 bps (0.25%) or 50 bps (0.50%). As of Wednesday morning, the odds stood at 81% for a cut of 25 bps and 19% for a cut of 50 bps. The Fed cut rates 25 bps on Wednesday afternoon.

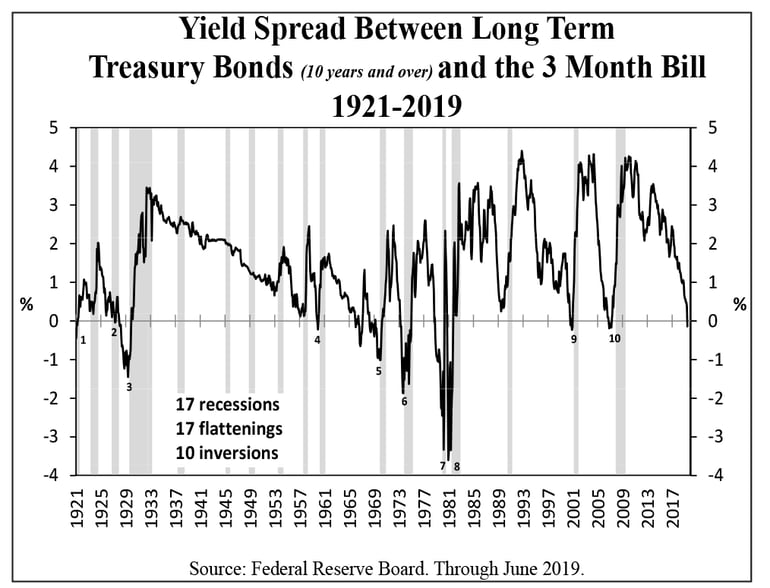

The chart below, from the brilliant Dr. Lacy Hunt of Hoisington Investments, suggests that the Fed is already behind the curve, despite whatever it may think. This chart shows that, since 1921, we are now experiencing only the 11th curve inversion between U.S. government bond yields of 10 years and 3 months. Stated more clearly, the yield on the shorter term 3-month government bill is above that on the longer dated 10-year note, which is rare. In all 10 prior occasions, recession followed within a reasonable amount of time. Why should this time be any different?

In prior recessions, once the Fed realized its mistake, it seems to have panicked and cut rates dramatically. Our current belief is that a similar error would elicit a similar response. Exactly when, and to what extent, we cannot foresee. That is one of today’s greatest points of uncertainty, and hence the greatest opportunity, in our opinion.

To me, the verdict of history is clear, even if the timing isn’t: recession may be closer than anyone expects. If so, the Fed should likely start cutting rates dramatically. It’s our expectation that it will, even if it does so belatedly. This, we believe, is one of today’s biggest problems. But today’s problems often turn into tomorrow’s most profitable solutions. We believe an investment in the mortgage REIT sector may be one such profitable solution.

“The stock market is a device for transferring money from the impatient to the patient.” – Warren Buffett

Historically, the equities in the mortgage REIT sector have responded very positively once it’s clear that the Fed is decisively cutting interest rates, often seen most clearly when the economy is in recession. Of course, to observers right now, it’s likely anything but clear that the Fed is aggressively lowering rates or that the economy is in a recession. But is that not the message of the almost 100 years of data in the chart above that inverted yield curves lead 100% of the time to recession? Ten for ten? Even though the timing is unclear? And should we not, as value investors, seek out investments where we are most compensated for the risks we take? Those with what we think are very high odds of success?

We believe, accordingly, that now is the time of maximum uncertainty for mortgage REITs. My experience is that maximum uncertainty often has a welcome side benefit: maximum undervaluation. We believe that this is a risk worth taking, one for which we believe investors are being compensated thanks to the 10% plus yields in the sector. This is our methodology as value investors – to look ahead to what we can credibly expect and be willing to suffer the indignity of uncertainty and even short-term loss while we await a more profitable future. We know, as should you, that there is no return without risk. This is a risk that we believe is worth taking, especially with historic odds of 10 for 10.

“Blessed is he who expects nothing, for he shall never be disappointed.” – Alexander Pope (clearly the first value investor)

A Key Principle of Our Valuation-Driven Investing is that Tomorrow’s Investment Winners are Often Today’s Most Obvious Losers. We Seek out Big Problems and Invest in Their Solutions.

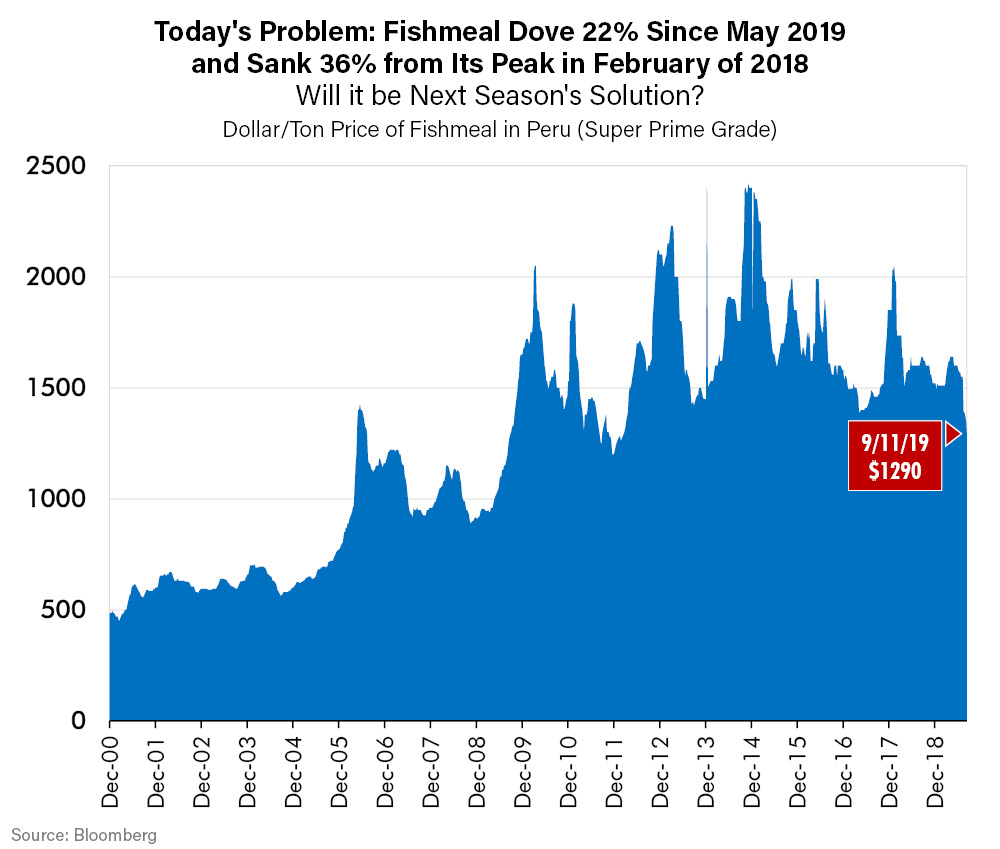

While on this topic of identifying today’s biggest problems, we wanted to highlight the disaster unfolding in a sector we have long monitored: fishmeal. Fishmeal is the world’s lowest cost animal protein, made from wild caught fish off the coast of Peru, Chile, South Africa, and the U.S. Gulf of Mexico. These fish, such as anchoveta, jack mackerel or other wild species have historically been key ingredients of higher valued added animal feed, used for the development of young pigs and increasingly for aquaculture (farmed fish).

The dominant flow of trade is from Peru, the Saudi Arabia of fishmeal thanks to the cold richness of Antarctica’s Humboldt Current, to China. Peru is the world’s biggest exporter and China is the world’s largest importer. China is gripped right now with what is quite possibly the biggest crisis in the history of pork. Estimates of loss from African Swine Flu run as high as 40-60% of the swine herd in China, by far the world’s largest. This unprecedented crisis is battering the fishmeal sector, with prices plummeting as demand from its biggest consumer collapses, as displayed below.

While today’s short-term fundamentals are now clearly devastating and getting worse, our experience has been that today’s problem can become next year’s investment solution. Remember that markets look ahead, so we may reasonably expect prices of investments to anticipate events, such as the eventual stabilization following a huge downcycle.

To profitably bridge the gap between a terrifying now and a more encouraging future, investors should do their homework to identify the companies that can most profit from a recovery – and be patient! The solution lies in the future, while the problem is now. We believe only patience – and proper analysis - can profitably bridge the gap between the two. To us, that is the definition of a successful investment. Most are impatient, after all the now is so terrifying! That is the opportunity for disciplined value investors.

We can never forget that the nature of unprecedented disasters is that they are rare! Today’s fishmeal apocalypse is rare. Today’s yield curve inversion is rare. That’s why we believe that they may lead to future opportunities. But we can never forget that cheap stocks can and quite often do get cheaper. We can mitigate that risk through security selection within the sector, finding investments with multiple ways to win and strong balance sheets. Portfolio construction too, can be our friend, with a diversified mix of investments.

Never forget that diversification means a diverse set of outcomes within the same portfolio. This means that not everything will work at the same time. Some will fall. Others will rise. Do not be surprised by this. Ever.

Our experience has taught us that the nature of cycles is that fundamentals mean revert, suggesting today’s bear markets can be tomorrow’s bull markets. So, from that point of the view, the bigger the problem, the better. We believe that the problems we have outlined today should see a similarly encouraging solution.

“We have neglected the truth that a good farmer is a craftsman of the highest order, a kind of artist.” – Wendell Berry

In Conclusion

We believe that thoughtful portfolio management demands patience and discipline. We often explain this with the analogy of a farmer and his seed corn, seed held back for planting next year. A shortsighted farmer who focuses only on today, would eat his whole crop and live like a king this year. The next year, he would starve. He has nothing to plant and nothing to harvest. Portfolio management is a lot like that. Today’s under-performing investments and distressed opportunities are tomorrow’s crop. Short term under-performance may be the price for not starving next year. Think about it.

As risk managers, we believe we must invest a portion of this year’s crop to plant next year’s harvest. Our goal is to never starve! As value investors, we should welcome pockets of extreme weakness today that our research has identified. Why? Because today’s undervalued opportunity may mature into next season’s crop and provide the next generation of seed corn. We view it as our job as value investors, to move from one problem to the next. The process is unending.

This means that a portion of the portfolio should always be in the most distressed situations of today, if this is where the best values are. Such investments can seem, in the short run, hopeless situations fraught with uncertainty. Of course they are! Is this not why they are cheap!? But our view should extend beyond this season to next season’s harvest too. Today’s lagging investment can be the seed corn for next season’s harvest. We should look to the future and invest accordingly, lest we run the risk of the short-sighted farmer who starves next season.