CHIEF CONCLUSION

In the last four years, there has been an $9.1 trillion increase in negative yielding debt. The total now is $12.8 trillion. What broader impacts has this driven in our markets – and what may be next? We think that gold may be a superior rival to assets that accept a negative return, even those that are widely considered to be “risk free assets.” Gold has no default risk and may grow in attractiveness as a diversification tool, especially given that total mined gold supply has expanded less than half a trillion dollars during the same time that negative yielding bond supply grew $9.1 trillion. Keep in mind, this growth in negative yielding debt our world has created in the last four years is greater than the value of all the gold mined in the world since the beginning of civilization. A little bit of bond money flowing out of bonds might go a long way toward pushing gold prices higher.

Yesterday was “Fed Day,” one of those periodic times when the leadership of the U.S. Federal Reserve comes out and discusses its short-term outlook for monetary policy. It’s around these days especially that what passes for financial TV gets clogged up with heads that talk only about the Fed. I can only imagine that they consult the stars to guide them in their interpretation of events. But, even if the stars don’t lie to them, and if their interpretation rings true, are we supposed to believe that this exercise adds value towards managing a portfolio thoughtfully towards a goal many years in the future? I suggest a more productive exercise is to turn off the television and do some real analysis. Sharpen your pencil and get to work! That’s what I did anyway.

One of the items I have been reviewing, is the tremendous explosion in the amount outstanding of negative yielding sovereign debts worldwide. The latest number is $12.8 trillion of negative yielding debt. Trillion with a “T!” This number means that close to 30% of developed market sovereign debts now have a negative yield. However, almost all this debt resides outside our shores, so I can understand how the concept of negative yields still sounds crazy to U.S. based investors. But I also think it is naïve to ignore the explosive growth in this negative yielding debt, from “only” $3.7 trillion in early 2016 to $12.8 trillion now. That’s a $9.1 trillion dollar increase in less than 4 years. Isn’t that incredible? At the same time, the increase in physical gold supply from the world’s mines was less than half a trillion dollars (92% slower supply growth in gold than negative yielding bonds in dollar terms). Hmm. What would happen if bond investors traded their negative yielding bonds for an investment in default free gold? How high would the gold price need to go to make room for them? That is the question we want to ask today.

I thought it might be useful to take a few minutes to talk about just what an unfathomable amount of money we are talking about. My goal is to try to make that number real and explore how this new and growing reality may up-end our markets.

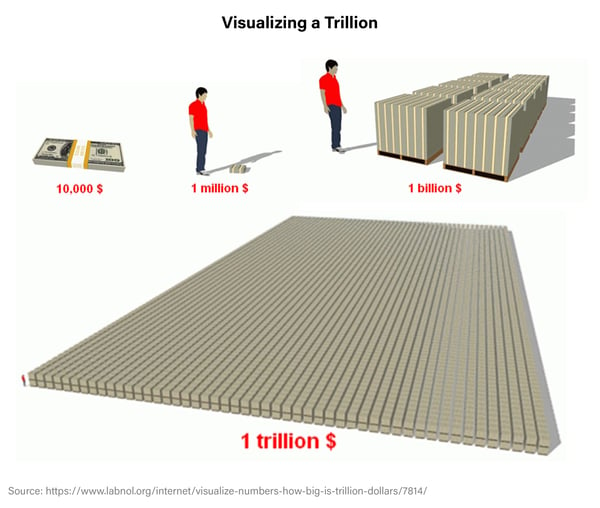

“A billion here, a billion there, and pretty soon you’re talking real money.” – U.S. Senator Everett Dirksen

Visualizing a Trillion

I remember the quote above from the 1960’s, back when a billion dollars was a lot of money. But, a trillion is a thousand times more than a billion. How does one even begin thinking about such enormous numbers? The images below may help. Look closely, and you can barely make out the tiny, person-sized figure at the bottom and left of the enormous rows upon rows of pallets of hundred dollar bills necessary to total $1 trillion. Now multiply this times 13. That’s how much negative yielding debt there is in the world.

Sovereign Bonds: From Risk Free Returns to Return free Risk

After the final remnants of the gold standard finally collapsed in 1971, the world appears to have adopted a system where sovereign debts became the reserve assets of choice. These assets backstop the world’s banking systems. Our modern financial system treats these bonds as the very apex of creditworthiness. I can understand that thinking, given the awesome sovereign power of the modern nation state to borrow and tax, and enforce its will upon its citizenry and its creditors.

For many years now, the yields on these sovereign debts have been widely considered “risk free rates,” meaning that their yields were the returns that investors earned when they sought safety. Arguably now that many yields are negative, these bonds could be said to present return free risks! How much the world has changed!

One could make a persuasive argument that, at least in most developed markets, these bonds delivered on being risk free returns. We have not been averse to owning higher quality, longer dated bonds, which have appreciated in price as global interest rates have fallen. These bonds have played a powerful role in portfolio construction by helping to diversify an equity-rich portfolio. So the goal here is not to bash higher quality, longer dated bonds. This falling trend now in rates, especially outside the United States, has dragged many yields not just low but negative. So how are we thinking about this now?

“It was a period [1932-1946] when a large part of the liquid capital of the country attempted to crowd into the always limited [emphasis mine] area of riskless investments.” – Sidney Homer, the Father of Bond Research

Many investors have already retired or are nearing retirement. This means, for most, that safety becomes more important and thus an investor’s risk tolerance goes down. Bonds, especially for these investors, have traditionally played a valuable role. After all, high quality bonds pay steady income and their more senior claim on a company’s or borrower’s assets give them a pattern of return that is often different from that in more risky equities, a junior claim. Retired investors in particular seem to value this diversification, because permanent capital losses may not be made whole by future earnings. The stakes are just too great. But what happens when rates go negative? What options should thoughtful investors explore?

Am I the only one that has been following recent political events with alarm? Next year may be one of the most pivotal Presidential elections in memory. The electorate is polarized and the choice is not likely to be between two centrist candidates, as it has usually been in the past. The party of the left in particular, shows that the proponents of the most radical socialist policies in eighty years are leading at the polls. No one can assure any of us that these candidates will not win. In my opinion, if you are not concerned by now, you are not paying attention. But frankly, the U.S. still looks like an oasis of stability compared to the rest of the world. Hong Kong appears to be an obvious example with even Chile, once considered a bastion of stability in Latin America, finding millions taking to the streets in protest of the status quo.

In the last few months, an explosion of civil unrest or outright riots has sprung forth throughout the world. The U.K. has been gripped in almost four years of Brexit-driven chaos and has been in and out of a constitutional crisis during much of this time. Closer to home, our own House of Representatives is driving a similarly chaotic political situation, with a process that is lurching toward impeachment. The point is that “sovereign stability” ain’t what it used to be. Yet trillions of dollars are invested in negative yielding debt, guaranteeing no return while facing rising risk. Is there really no better way?

Supply and Demand: Gold vs. Sovereign Debt

Our long experience has taught us to always analyze supply and demand. Do the math! The supply of negative yielding debt since early 2016 has expanded by 13 times as much as the available gold supply from the world’s mines in dollar terms. In fact, it has grown more than the entire amount of gold that has been mined in the world since the beginning of history! Let that sink in for a moment. Governments created negative yielding liabilities, in less than four years, in more than the amount in dollars of all the gold ever mined in the history of the world. Are you paying attention now?

The largest quarterly expansion of negative yielding debt (so far) was Q1 2016 when the supply expanded by $4.9 trillion. The largest quarterly expansion of gold supply has been less than 1/100 of that at $40 billion. Since 2016, the incremental demand for gold in the world’s ETFs has been less than 1% of the incremental value of the negative yielding debt growth. What would the gold price look like if that percentage doubled to 2%?

Looking at it another way, assume only 1% of the value of negative yielding debt was moved into the world’s gold ETFs, that would be $128 billion of new demand for gold, more than an entire year of new mined gold supply and more than all the gold currently in those ETF’s. This is a potential supply/demand mismatch worth pondering.

If both sovereign debt and gold have no yield, which one would you rather own? I view gold as a potential superior substitute to those trillions of dollars of negative yielding debt, because gold may not yield anything, but that is more than a negative yield and it has no default risk. The same cannot be said with certainty of any bond in the world.

“Anyone can hold the helm when the sea is calm.” – Publius Syrus

In Conclusion

Can anyone survey today’s world and feel confident that they fully understand it? Negative interest rates, political unrest, a global crisis in government legitimacy?

For the last ten years I have prioritized the study of how to navigate a world of increasingly polarized and radical politics. In the aftermath of the Global Financial Crisis, I reached the conclusion that the world’s voters had unfinished business with their ruling elites. Current events have not disappointed.

Political unrest and its complications have consumed my waking thoughts since 2009, just as much as the study of credit did from 2006 to 2007. I am a firm believer in educating myself to understand, if I can, the nature of the world I expect to see. Certainly I can’t fathom how investors could face today’s markets without such a program of dedicated study. If your “plan” is to just roll out of bed and figure it out as you go along, good luck with that.

I think a lot about what may happen, which means thinking through potential scenarios such as I outline above. I am certainly intrigued about the potential demand for gold as a substitute for negative yielding bonds. It’s hard to say exactly what this would mean for the price of gold, but my best guess is higher.

When I look at today’s world and speak to investors, I see a great longing for “safe” investing. Investors know that without risk there can be no return. But many share a sneaking suspicion that something is off in the world, and they can’t quite put their finger on it. Confidence in the old rules is not what it used to be. This means, I believe, that the stakes have never been greater for investors. Negative interest rates are possibly just the weirdest of the paradoxes we face.

Our conviction is that disciplined research and patient investing is the best answer to the challenges we face in the market. Our suggestion is to turn off CNBC and pick up a calculator. Watch less TV and do more math. Consider how the world is changing, and what that means for diversification in an ever more confusing world. The math of negative yielding bonds versus gold, in particular, is worth considering. It’s sobering. The future is coming. Are you ready?