The rainy season is well underway here in sunny South Florida. Each day I can confidently predict that the weather will be hot and humid with a good chance of afternoon showers. I can even track by the very minute the progress of the most menacing storm clouds thanks to the wonders of the internet. With one eye fixed upon the thunderheads as they barrel over from the Everglades, my family can enjoy the outdoors and slip inside just ahead of the afternoon deluge. Such dependable weather patterns and reliable near-term forecasting make planning easy. And we think nothing of it.

But how amazing would it be to forecast the economic cycle with such clarity? Now that would be something! How much easier would it be to manage an investment portfolio, owning the right assets at the right time? Aggressive investments would take place at the economic trough to harness the power of the cycle, transitioning into more defensive investments at the peak - just ahead of the storm. Rather than fear the cycle, its volatility would be welcomed as a trusted friend and partner. Many are the investors who wish they had not gotten the cycle wrong, especially when the punishing downturns of the U.S. housing and Global Financial Crisis from 2007 to 2009 seemingly “came out of nowhere.”

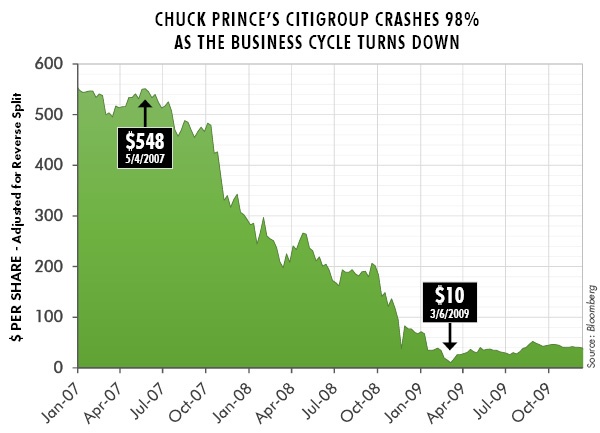

Our understanding of economic cycles has lagged badly behind the tremendous progress in understanding and forecasting the weather. Can we really do no better? Even if perfection is elusive, is it worth trying to be roughly right – as Keynes noted? Especially when the alternative – getting crushed by the cycle - is so costly? I think if we asked Chuck Prince and his shareholders from 2007 to 2009, they would answer “yes!”

Many indeed are the executives and investors who have been humbled by the business cycle. Perhaps none has suffered more publicly than Chuck Prince, the CEO of Citigroup. In mid-2007, early into the first stages of the financial crisis, the leadership of Citigroup badly misjudged the impact of the unfolding business cycle. The downturn would begin in subprime mortgage debt but would soon broaden far beyond that sector. Citigroup had misjudged where it was in the cycle and thus was carrying far too much financial leverage to safely weather the storm. These mistakes would cost Citigroup's shareholders dearly, as the chart below demonstrates.

To this end, to the study of cycles and their impact upon the financial markets, have I dedicated the last fifteen years of my life. Although I have much yet to learn, my studies have uncovered a few key principles and milestones that may prove useful in avoiding the pitfalls that claimed Citigroup in 2007. In today’s “Trends and Tail Risks,” I share what I have learned about the business cycle and how thoughtful investors may profit by harnessing its volatility.

Clément Juglar: Father of the Business Cycle

Clément Juglar: Father of the Business Cycle

Clément Juglar was a Frenchman, born in 1819, into the long and storied French tradition of Renaissance thinkers. He began his career as a physician but would be best remembered for his works in economics. His research in the late 19th century would be among the first to study and characterize the drivers and cyclicality of the economy. Joseph Schumpeter, one of the most respected economists of the 20th century, would call Juglar “one of the greatest economists of all time.”

Juglar was an empiricist. He gathered exhaustive data covering a broad host of economic series in many different countries. From his study of the data, Juglar identified a 9.5 year average cycle that now bears his name. Juglar hypothesized that alternating periods of over and under investment drove this cycle. Investment is driven by confidence and is facilitated by credit. The interaction among confidence and credit make investment the most volatile of all the major components of economic growth.

There are two subdivisions within investment. The first is a company’s investment in inventory. I have frequently outlined in these pages how changes in inventories drive the “unexpected” volatility of the Kitchin Inventory Cycle (“Making Volatility our Friend: Trading the Kitchin Cycle”, 05/28/14 and “Unsustainable Steel Premiums”, 09/03/14). These Kitchin cycles are shorter-term (36-40 month) cycles and, while often violent, may find balance more quickly than longer-lived Juglar Business Cycles.

The second subdivision of investment is in fixed assets. These include spending on property, plant and equipment necessary to expand a company’s physical production base. Fixed assets also include investments in residential or non-residential construction. These fixed assets are clearly much longer-lived assets than inventory parked temporarily on a company’s balance sheet. Company management teams must make long-term forecasts of supply and demand before making such long-lived investments. Sadly, these forecasts are built upon assumptions which future events may prove to be wrong and jeopardize the underlying economic returns of such investments. These errors make business cycle downturns longer and stronger than Kitchin Inventory Cycles. In fact, one may easily see this pattern of major Juglar Business Cycle downturns roughly every ten years starting in the post-1987 Crash downturn, the 1998/2000 Asian Crisis and post Tech Boom crash, and of course the 2008 Global Financial Crisis. The most violent down cycles of all happen when the Kitchin and Juglar cycles overlap and reinforce each other to the downside like they did in 2008.

Juglar identified a long prosperity whose peak was marked by a credit panic, as creditors lost confidence in prevailing values and in future prospects. This loss of confidence would spark the liquidation phase of the cycle which purged the system of prior flawed decisions and distended values. It’s important to note that the credit panic did not cause the down cycle. Juglar’s view was that the down cycle was an inevitable and even healthy part of the business cycle. Juglar believed that the seeds of the downturn were already sown thanks to poor decisions made along the way during the prosperous phase of the cycle. The credit panic only served to reveal these bad decisions and overvaluation.

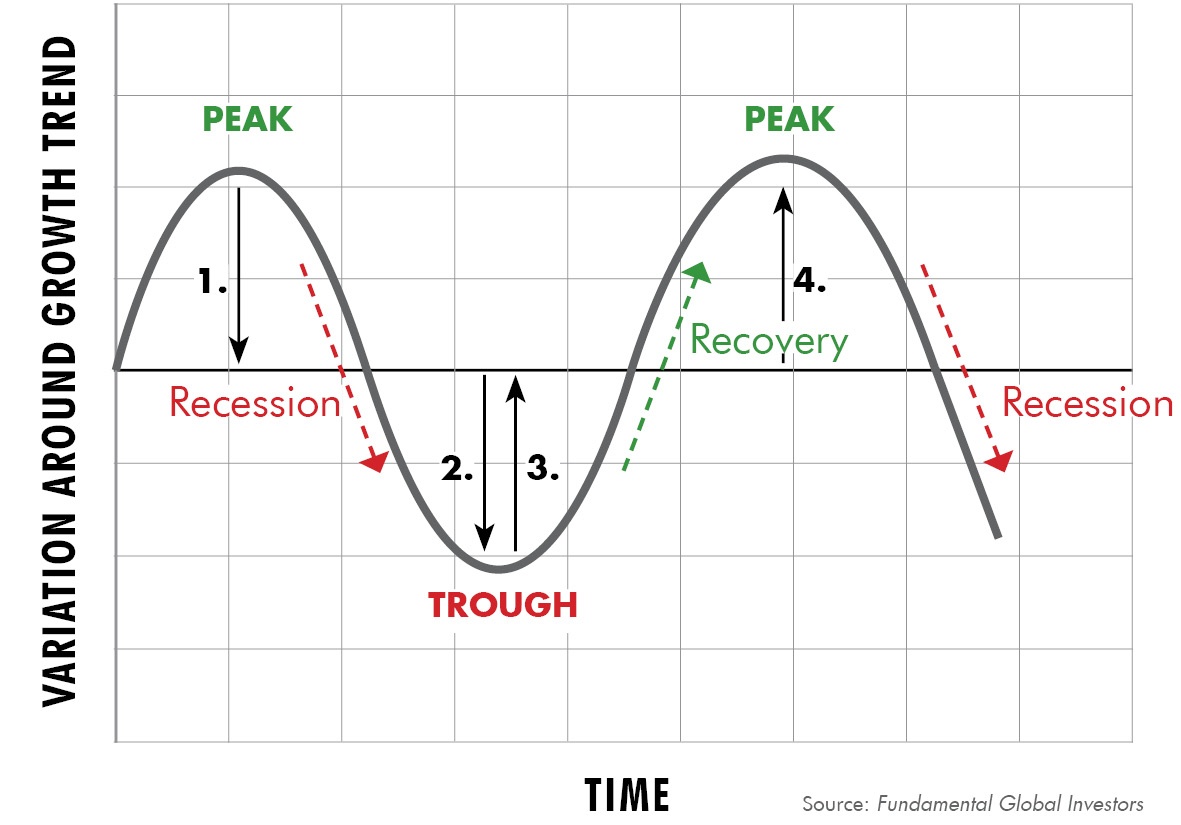

As the chart above illustrates, there are essentially four phases to the business cycle: (1.) from the peak of prosperity into a decline toward recession, (2.) a recession of negative growth from the liquidation of bad investments that ends with a trough, (3.) a time of recovery out of the lows of the trough, culminating with (4.) a strengthening recovery that ends with a peak of prosperity, often ended by a sharp down cycle (panic) in the credit markets. Each phase of the cycle breeds the necessary preconditions for the following phase. The cycle is not complete without all its phases.

One of Juglar’s key insights was that investors and capital allocators often become unduly optimistic near the peak and act upon this over-confidence by borrowing through the credit markets to overinvest in fixed assets. Over-confidence and a peak in credit naturally go together. Credit flows in the near term actually serve as added fuel to the economic fire, naturally self-reinforcing each other in a way that George Soros has called “reflexive.” Taken to an extreme this self-reinforcing phenomenon can create a mania where commonly held views take hold and drive asset values and the fundamentals related to them far over their equilibrium value in the upcycle, and far below their fair value in the down cycle. As a value investor, I can use the volatility of this cycle to profit when investors lose sight of a company’s true fundamental value (“From the Analyst’s Toolkit: Replacement Cost Valuation”, 06/11/14).

Juglar’s analysis laid the groundwork for how a panic in the credit markets is so often the catalyst for a down cycle. Credit is the means by which economic actors can consume or invest more than their current cash flows will support. So credit is a key facilitator of growth that can soon run to excess. As doubt re-enters the mind of lenders, borrowers find it very difficult to get new credit. As credit growth slows, the growth that credit made possible slows as well or even reverses. Credit’s key role in the business cycle is one of the reasons that I so often focus on the underlying health of the credit market (“Market Raids and Weak Links”, 10/22/14; “The Debt Hurricane”, 01/14/15).

One of Juglar’s many contributions to the study of cycles is his conception that cycles in economic activity are normal and even healthy. Cycles contain within themselves the causal drivers that move asset prices over time toward fair value. Short-term factors may drive asset values to exuberant prices into the peak and suppress values far under fair values into the trough. But longer-term values are the equilibrium level sought out by all the forces of the cycle acting together (“Prices Allocate Resources”, 06/25/14).

Looking Forward: Thinking about the Juglar Business Cycle

The Juglar Business Cycle averages 9.5 years in length, with of course a degree of variation around that trend length. This suggests that the most logical window for a peak in the business cycle remains well into the future, around an expected date of late 2016 into 2017. However, many forces are always at work that may draw the Juglar Business Cycle to an earlier – or later - conclusion. Certainly when I survey the world I see no shortage of credits about which to be concerned. Greece, for instance, is a meaningful problem for the credit markets about which I have written for more than a year (“Big Problems Start Small”, 05/21/14; “Greece: The Bank’s Problem”, 02/11/15).

So while reasonable people can certainly disagree about the specific locus and date for the future peak in the business cycle, there are a few generalizations I can make. I can confidently anticipate, for instance, that credit problems will be the key catalyst for a peak in this cycle, just as credit has been at the heart of major turns in past business cycles. Oftentimes the emergence of a peak comes as a rolling series of data points, much as it did during the last cycle.

The most important of the signposts last cycle were (1.) An inverted yield curve in February 2006, (2.) a sustained turn higher in credit default swaps (CDS) in high yield in February of 2007, and (3.) the clear inflection point in July 2007 when a deep loss of confidence in the once-booming market for subprime mortgage backed securities exacerbated what had been a lingering credit malaise. The relative value of gold also confirmed the importance of the turn in July 2007 by strongly outperforming other asset classes (“Gold: Price vs. Relative Value,” 07/23/14). I monitor these and other indicators constantly to avoid complacency about the Juglar Business Cycle. Many of these indicators I have discussed in previous publications ("Is Credit Quality Peaking?”, 08/06/14).

U.S. Credit Markets: Will the Confidence of Today Sow the Seeds of Future Problems Tomorrow?

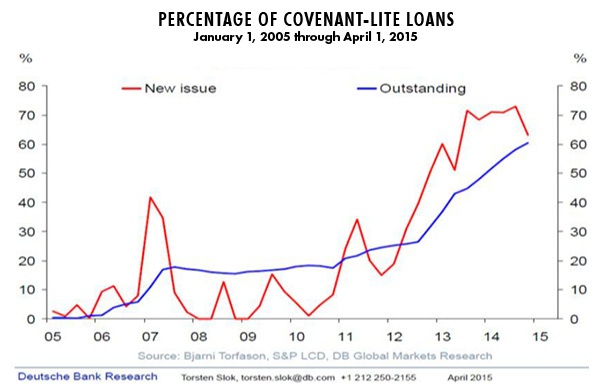

Signs of credit excess, the credit markets that are most ebullient, are very often ground zero for identifying future peaks in the business cycle. Sadly, I do not have to look very hard to see the outline of future problems that the market will “discover” once the business cycle peaks. Recently, savvy bond investor Jeff Gundlach of DoubleLine used the chart below to demonstrate the dramatic decline in the quality of recently issued debts. His chart draws upon research by Deutsche Bank which shows an alarming increase in “covenant-lite” loans both as a percentage of newly issued loans and as a percent of total credits outstanding. “Covenant-lite” loans are those that lack many of the traditional safeguards upon which bond investors once counted.

Gundlach’s concerns – and mine too – are not so much about the market right now but are more to do with the future. The fear that we both share is that such weaker credits may prove more subject to stress in a future cyclical downturn. If so, once again developments in the credit markets will prove to be at the forefront of understanding the Juglar Business Cycle.

In Conclusion

In days past economic scholars such as Clément Juglar worked to benefit mankind through the study of economic cycles. The very foundation of economics was laid by such pioneers who sought to study the world as it is in order to better understand how to avoid its dangers and profit from its successes. Those days are sadly long dead. Economics today has largely abandoned its roots in the study of real world cycles. Now endless quantities of ink are spilled generating a never-ending supply of dense papers on useless topics that few read and even fewer understand. What a wasted opportunity!

I believe that there is a clear unmet need for the serious study of economic cycles and the damage they may cause. My own experience as a professional investor has demonstrated the merit of understanding the causal drivers of cycles to avoid painful mistakes and even profit from the market’s temporary mis-pricing of assets. This belief is a core tenet of my thinking and lies behind the publication of this weekly.

It is unacceptable that in this day of modern marvels that economists’ understanding of economic cycles is so completely backward and undeveloped, especially when its impact upon wealth and prosperity can be so devastating. The contrast between the science of weather forecasting and economic forecasting should be a call to action.

Perhaps economics lost its way because it has seemingly embraced an endless faith in governments and central bankers and planners? But has the rise of government and the ascendancy of central bankers banished all economic volatility? Surely not! Until the day that our central planners finally deliver utopia, it is up to each one of us to educate ourselves. Harnessing the power of the cycle’s volatility is neither simple nor easy. But can anyone dispute its benefits in heartache avoided and money saved? •