There are many challenging aspects of investing. Perhaps in no other field does the oppressiveness of the unknown cast such a long shadow as over our efforts to safely shepherd capital through an uncertain market. The heart of our challenge is this: the markets are forward looking and anticipate future fundamental events. How can we successfully invest today to profit from an uncertain future tomorrow?

Of all the challenges that stem from this dilemma, there is none more finely balanced on the razor’s edge than the judgment call: when to double down on a loss-making investment and when to cut losses and move on? Spend enough time in the markets and I promise that you will stare into the abyss of this dilemma. The world’s finest investors, the truest practitioners of our craft, have proven their ability over time to make the right decision and profit from it. Some of my most trying – and profitable - times as an investor have been when I have successfully wrestled with such a decision. How can we learn to make better decisions? I believe that replacement cost valuation can be our most trusted guide. This week’s “Trends and Tail Risks” explores this topic further.

Reality May be a Function of Viewpoint: the Art of Shigeo Fukuda

Japanese artist Shigeo Fukuda pursued an interesting art form that may shed some light on how we try to profitably make the hardest judgment calls in investing. Shigeo Fukuda was born in 1932, and in 1956 graduated from the Tokyo National University of Fine Arts. Fukuda first rose to fame through his innovative poster design. As his craft matured, his art expanded to show us images we thought we understood, and helped us to see and to understand them in a new way.

One of the most striking examples of his work is below, “Lunch with a Helmut on” from 1987. Fukuda painstakingly crafted the sculpture below out of 848 knives, forks, and spoons. When viewed from one angle, his work seems merely a shapeless mass of cutlery, but when viewed from another angle, his sculpture casts the perfect shadow of a motorcycle! Each wildly different image comes from the same object. His sculpture shows us two totally divergent yet simultaneously valid images at the same time! What is the truth? The sculpture? The shadow? Both? Neither!?

Illusionary Art & Design.

Left: Shigeo Fukuda - Graphic Artist Right: "Lunch with a Helmut On," 848 welded Forks, Knives & Spoons, 1987 Fukuda wanted to create a three-dimensional object in which the shadow, as opposed to the actual form, represented the object.

Source: Masters of Deception, by Al Seckel, 2004

Applying this Lesson to Investing

I am fascinated by Fukuda’s work because it hints at a profound truth in investing: sometimes the same experience can mean multiple things, each valid in its own right. For instance, as I outline in the case study below of replacement cost investing, one of my most successful investing campaigns ever actually began as my worst. Let me explain.

Frequent readers of this weekly will understand that replacement cost is one of our favored valuation metrics (“From the Analyst’s Toolkit: Replacement Cost Valuation”, 6/11/14, “Seeing the Ball” Clearly: The Value of a Cogent and Controversial Narrative," 4/15/15). The replacement cost of a company is essentially the cost to recreate a company’s existing asset base. One might think of it as “true” book value, or as book value marked to market. We use replacement cost valuation because it helps us to never forget that a company is simply a body of assets moving through time. As the body of assets approaches the peak of a cycle, the same assets become more profitable and earnings rise. As the body of assets approaches the trough of a cycle, the same assets yield lower earnings. But the constant throughout is that a company’s asset base itself does not really change that much. We use the discipline of replacement cost valuation to avoid overpaying for assets at the peak of the cycle and to cheaply purchase assets at the lows of a cycle.

A Historic Example: Learning from our Mistakes

As 2003 began I was an enthusiastic shareholder of a company called IMC Global, the world’s largest phosphate fertilizer operation and one of the world’s largest miners of potassium chloride, a key plant nutrient. I had found the company by focusing my valuation work on beaten down and horribly underperforming sectors of the market. Almost no sector had performed as poorly as the fertilizer sector had over the prior decade. With a collapse in the cycle had also come highly depressed stock prices, and therefore - compelling valuations. I became the largest shareholder in the sector, owning big stakes in all the major players. IMC Global was my last purchase in the group. According to my valuation work, the company was trading at 40% of the replacement cost of its underlying assets, making it the cheapest stock in the sector among the major players. However, I still had a lot to learn about using replacement cost as a tool – as I would soon find out to my dismay.

In fact, the stock quickly tumbled 50% over the next few months. What happened? I had made a number of costly errors, each of which makes me cringe today when I think back upon them. I had not understood where we were in the inventory cycle ("Trading the Kitchin Cycle," 5/28/14), so I naively accumulated the stock just ahead of the strong downcycle phase into the inventory destocking trough. This “unexpected” slowdown stressed all companies in the sector, but none as much as IMC Global, which was particularly vulnerable for two reasons. The company was not a low cost producer but rather was relatively high cost. This was bad because in a downcycle prices often fall low enough to make all but the lowest cost producers unprofitable. So all assets were not created equal. Low cost assets were definitely better. That is not what I owned in IMC Global. I was taking more risk than I realized.

Furthermore, the company’s debt level was fairly high after a series of ill-timed acquisitions. High financial leverage on a relatively high-cost producer can be an especially toxic combination when the cycle turns down. IMC Global’s debts could (and did) get downgraded as fundamentals weakened. The company responded by issuing shares at a very distressed valuation, diluting its equity shareholders, to satisfy worried creditors.

Reflecting back, I frankly should have been more focused on the company’s balance sheet from the very beginning. In a replacement cost calculation, one calculates the value of the company that belongs to the equity holder only by first subtracting out all the company’s debts from our estimates of replacement cost for the assets. So the equity of a highly indebted company may suffer disproportionately the burden of a valuation decline, often seemingly out of proportion to the extent of the fundamental challenges the business faces. This is so because our analysis values the company as if we were liquidating it: subtracting out the value of the debt from the value of the assets, repaying the debt in full, and keeping the remaining value for shareholders. So it was the equity tranche of the company’s capital structure that bore the full weight of the deteriorating fundamentals. Small declines in replacement cost valuation can be quite damaging to equity values when debts are large.

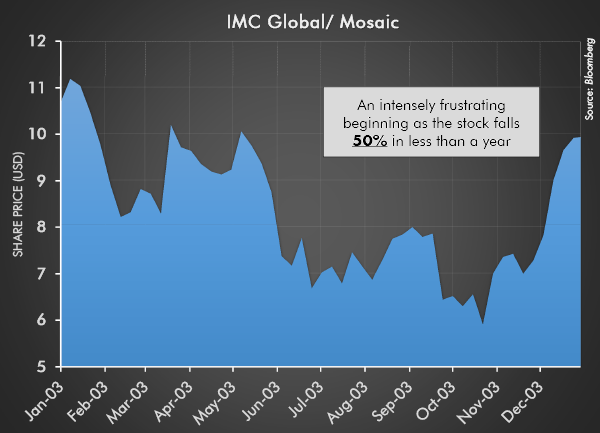

Viewed from the Perspective of Mid 2003: A 50% Loss

I had unquestionably suffered through one of my worst performance periods ever. That was just a fact. The stock had fallen 50% by mid-2003. What had seemed like a great investment trading at 40% of replacement cost was now trading for an amazingly cheap 25% of replacement cost. What to do with the stock now? The choice I faced was this: to sell and recognize our substantial losses – or to buy more? I deliberated for many long and stressful days about the proper course of action. My decision was to buy more. My line of thinking went as follows.

With the stock trading at $5/share I could still drive an upside price target of nearly $30/share. While my earlier investment had unquestionably lost money, I knew that at the depressed price I still had multiple ways to profit from my investment. I also had less downside risk for new investments because the stock’s decline had already substantially lowered my risk of further loss even in a worst case scenario. The decision to buy more was not an easy one. I lost a lot of sleep over it. And it was not driven by stubbornness but rather a dispassionate conclusion about how much I could make if I was right relative to how much I could lose if I was wrong.

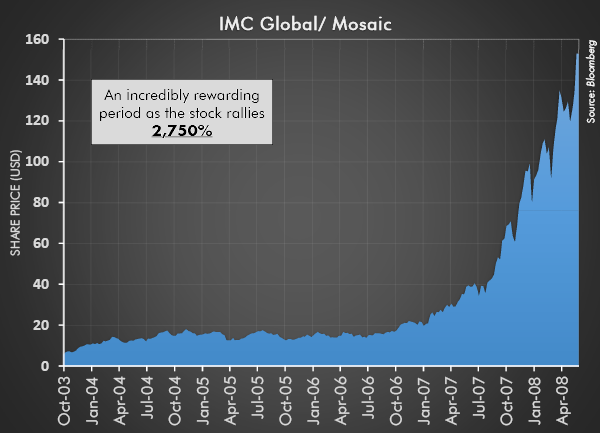

Viewed from the Perspective of Mid 2003 to 2008: a 2,750% Return

It was certainly never in my wildest dreams to imagine that my worst investment ever would turn into one of my best investments ever. One of the most important tenets of value investing is that future returns are a function of how cheaply we buy our investments. And at 25% of replacement cost IMC Global was an amazingly cheap stock.

Furthermore after long experience I have now come to realize that just as it’s possible for everything to go wrong, it’s also possible for everything to go right. Agricultural commodity prices rose dramatically, increasing the demand for the company’s fertilizer nutrients. Growing demand consumed the world’s excess supplies which dramatically increased fertilizer nutrient prices. President Bush would subsidize ethanol production to turn corn into fuel. The agriculture sector would command center stage – with the once downtrodden fertilizer sector at its very epicenter. How radically had the world changed in just a few years! Not even the most optimistic of investors could have foreseen just how good things would get.

But the path upward was definitely uneven. IMC Global would stumble through and be acquired by its competitor Cargill, who gained two thirds of the new company Mosaic (MOS) even though Cargill only contributed one third of the new asset base. That was the power of Cargill’s stronger balance sheet and the savvy deal-making of the man who ran its fertilizer business, Fritz Corrigan. There would be other destocking cycles along the way that would interject uncertainty and create fear before the next upleg could resume.

Many of those who invested with me in the stock would remember fondly the nearly 30 fold rally that the stock enjoyed over the next five years. Not me. The initial 50% decline in the stock is what I can never forget. I cannot shake it to this day.

Still, there would be many benefits to my experience as I learned – the hard way – a few very important lessons that I still retain and apply today when using replacement cost valuation. Would Shigeo Fukuda see it the same way? Would he view this experience as analogous to his sculptures: representing at the same time both a huge failure and an important win? Somehow I think he might.

In Conclusion: Investment Implications for Today

We are constantly adding to the stable of undervalued equities that we own. We now find them globally in rayon fiber, iron ore (“Eyes on the Prize,” 5/20/15), and a number of other sectors that we will outline in future research reports. One of the key lessons we have learned since our experience back in 2003 is that we must buy and then patiently hold through the inevitable pushbacks that we can expect to encounter along the way. Odds are, we will be early. Odds are, unexpected events will threaten our investment thesis. To increase our odds of success we must take care from the very beginning that our investments are with low cost producers with good balance sheets who can withstand whatever the cycle can throw at them. Replacement cost valuation must also be our constant guide.

Other lessons include the importance of low valuations in driving industry consolidation. When we own low cost assets that trade at a big discount to their replacement value, we can make money through mergers and acquisitions even if the cycle’s improvement takes longer than we think. Executives in each sector understand the cost to expand their production footprint through capital expenditures which they make at full replacement cost. These executives also are not slow to move if they may purchase at a discount, in the stock market, that same production capacity in the form of a publicly traded competitor. In doing so, they may expand capacity more cheaply while also reducing competition in their sector.

A key part of our confidence in cyclical investing resides in the market’s unerring ability to use price to fix imbalances between supply and demand ("Prices Allocate Resources," 6/25/14). Downcycles do not last forever – nor do upcycles. Ultimately patience and a large dose of humility are the final key ingredients to successfully investing. Replacement cost valuation involves a trade off: we as investors agree to assume the risk of volatility while we wait, as well as the risk that comes from facing an uncertain future. After all, the distressed, ultra-low valuations that we seek are often only found in the sectors where a series of unexpected disasters created far more disruption and downside than almost anyone had anticipated. So the outlook for near term news is almost always grim. However, we are more than sufficiently compensated to assume these risks if we can purchase low cost assets with a good balance sheet at a large discount to the replacement cost of the underlying assets. This cheap valuation is our margin of safety.

I am now well into my second decade of using replacement cost valuation to trade more than a hundred different cycles in almost every sector one could imagine. The key tenets are always the same. Only the sectors and the dates are different. Our faith remains in the market’s ability to use prices to solve problems. Once we take the time to master these few key eternal truths that guide prices along their journey, we can reasonably expect that our patience and effort may be rewarded. Just because this is simple does not mean it is easy! Thankfully replacement cost valuation is a tool to guide our thinking through volatile times. And we have the lessons of history – and the art of Shigeo Fukuda – to help us understand that what may at one time be a failure can also be a success! •