Cycles are a prominent factor in much of our research on commodity driven companies. This is no accident. Commodity markets are always seeking balance between the fundamental forces of supply and demand. However that doesn't mean that markets are always in balance! Far from it. Major inflections in commodity markets can seemingly come out of nowhere. Investors can use that volatility to their advantage - if they remain focused on the causal fundamentals that make these events happen. We use our knowledge of cycles to force ourselves to remain open minded at potential inflections and to keep our research process very data driven.

In today’s Trends and Tail Risks we update our previous research in steel (Making Volatility our Friend: Trading the Kitchin Cycle, May 28, 2014) to analyze why the US steel cycle may be peaking and the effect this may have upon US based equities whose earnings are tied to the fluctuating steel markets.

We have been watchful for an inflection in the steel markets for the last several months because we are now fully in the window of time where it is logical to expect, based on historical norms, that excess steel inventories may be building in the US. The 1926 work of Joseph Kitchin outlines a cycle of approximately 40 months (measured from peak to peak and trough to trough) during which inventory levels fluctuate. High and rising prices are the mechanism by which the market gets its message across that industry participants are seeking to build inventories. The last such peak happened 42 months ago.

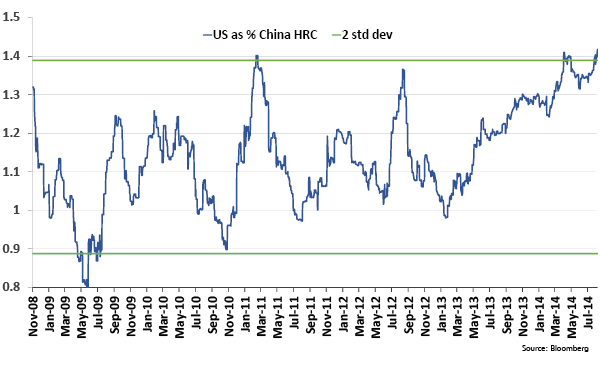

The chart below illustrates this peak by dividing the US price of hot rolled coil steel by the price of the same steel in China. We have also included the upper and lower bounds of this price relationship with a two standard deviation band showing the point at which the odds of mean reversion become overwhelming (45x1) according to the bell curve of probabilities. The odds now heavily favor the premium of US steel prices falling relative to those in China. US prices are also near historic highs relative to those of competing producers in the Black Sea and in Europe, which are historically large exporters of steel to the US. As such, the issue at hand is not an unsustainably low Chinese price. Rather, the key mispricing is an overly generous US steel price that incents lower priced steel to flow into the higher priced US market. These flows are the causal factor that ultimately overwhelm demand and result in excessive inventories that can only be reduced by the market lowering the premium of US prices over the rest of the world. The elimination of the premium price in the US will create the falling supply necessary to get inventories back to normal levels. The risks for US steel producers are compounded because China’s steel exports are expanding as Chinese raw material costs are falling.

We use general rules such as the periodicity of the typical inventory cycle to be sure that data, and not un-grounded opinions, drive our investment view. This is not a ‘macro’ observation. Price as the allocator of resources is the application of the laws of microeconomics that we all learned in college. Markets balance supply and demand and use price as the mechanism to do so.

The market has no more powerful a force than the incentive of a profit arbitrage whereby goods that are substitutes flow from a low priced region to a high priced region. The market enforces this law across many different sectors, not just steel. We use our understanding of this law to avoid getting caught up in the euphoria of a rising cycle when the news is good (and equity valuations are rich), and to help us spot bargains when the news is bad (and equity valuations are low). Our investing is never guided by our view of the cycle alone. At all times we exercise our disciplined valuation process by which we seek to secure a margin of safety in all our investments. We believe that to understand the interplay of valuation and the forces of mean reversion in markets makes us better informed, and thus more successful, investors. •