CHIEF CONCLUSION

Investments that could be considered “safe” have changed over time. One key driver of this change is how our financial authorities, in particular the world’s central bankers, have chosen to react to developments. When confronted with unexpected economic weakness, these central bankers cut interest rates. Falling interest rates are good for the prices of the highest quality, longer duration bonds. This has historically made them especially appealing to own in an equity rich portfolio. With U.S. equity markets at new all-time highs, we believe that now is an excellent time to begin rebuilding such hedges in the fixed income markets. We are trying to buy our winter coat in the summer! When it’s on sale.

Walter Bagehot (shown to the left) was the London-based Editor of “The Economist,” the leading global financial publication of his day in the 1860s and 1870s. Of course, Britain was the financial capital of the world back then. To its credit, this worthy publication is still available today in both magazine and online form and is an excellent summary of globally impactful political, economic, and financial news and analysis. Understandably, Bagehot’s vantage point gave him unique insights into the financial markets. This proved especially fruitful as he had a ring-side seat for the Lehman Crisis of his day, the collapse of Overend, Gurney and Company. When this bank failed in London in 1866, it sparked the largest financial crisis in decades in Britain and impacted the global financial markets in ways that persisted for years.

Walter Bagehot (shown to the left) was the London-based Editor of “The Economist,” the leading global financial publication of his day in the 1860s and 1870s. Of course, Britain was the financial capital of the world back then. To its credit, this worthy publication is still available today in both magazine and online form and is an excellent summary of globally impactful political, economic, and financial news and analysis. Understandably, Bagehot’s vantage point gave him unique insights into the financial markets. This proved especially fruitful as he had a ring-side seat for the Lehman Crisis of his day, the collapse of Overend, Gurney and Company. When this bank failed in London in 1866, it sparked the largest financial crisis in decades in Britain and impacted the global financial markets in ways that persisted for years.

Bagehot drew upon his observations of this crisis to publish what would be his landmark work, “Lombard Street: A Description of the Money Market.” In particular, this work would come to be the bible of risk management for central bankers in their role as “lenders of last resort,” meaning they were a source of liquidity for market participants during a panic when liquidity was unavailable. From that day and for the next 140 years this thinking would guide the behavior of central bankers - until the collapse of Lehman threatened to take down the highly interconnected global financial system and panicked modern central bankers into changing strategies. Before we talk about what changed, lets first take a minute to understand how things operated for more than a hundred years.

Bagehot’s conclusion was that the best way for a central bank to deal with a crisis of confidence was to lend freely and early against the best collateral - at high rates of interest. The goal of this strategy was to provide liquidity but also facilitate the needed economic adjustment that the unfolding crisis had revealed, hopefully in an orderly manner. This incremental liquidity would buy time for the needed readjustment. Implied in his counsel of lending at high rates was to discourage what would come to be known as moral hazard, namely that a central bank “rescue” would reward bad behavior that led to the crisis in the first place. Bagehot’s counsel signified that he believed that high interest rates had an important role in discouraging moral hazard because the central bank’s high rate would incent market actors to find lower cost sources of liquidity from the private market if it could be found. Nonetheless, the central bank should stand ready to provide the necessary liquidity at this higher rate against the collateral of the highest quality securities, in the event that insufficient liquidity was available from private sources. So, even though Bagehot clearly endorsed the need for “activist” central banking during a crisis, his suggested strategy was structured to minimize the risk of moral hazard. His focus on managing moral hazard was a key part of central bank thinking – until the failure of the Lehman overwhelmed it and marked a sea change in 140 years of central banking policy.

Lehman's Collapse Threatens the System: Central Bankers Abandon all Pretext of Fighting Moral Hazard

I am often asked what insights made it possible for us to dramatically outperform in the unfolding carnage of the Global Financial Crisis sparked by the failure of Lehman Brothers. Our early focus on the leveraged real estate market and the problems that would flow from its decline was one key insight. Another, which is more germane to this discussion of moral hazard, was that we knew something that our central bankers did not. We knew that the vast web of global overindebtedness and these interconnected liabilities made the system shockingly fragile and prone to collapse. This discovery, sadly, was late in coming to our central bankers and played the key role in explaining why they were so late to acknowledge and respond to the crisis.

Furthermore, the memoirs of crisis actors such as Treasury Secretary Hank Paulson and Federal Reserve Chairman Ben Bernanke – which I re-read this weekend - both reveal how obsessed they were leading up to Lehman’s failure with avoiding one form of moral hazard, bailouts. In the end, however, their worry about the system’s collapse clearly overcame their fear of moral hazard, as the subsequent bailouts illustrated. The crisis sparked by Lehman’s failure got their full attention, very late in the downcycle. And they threw out the rulebook that had worked for 140 years. Then a new era began, which is still in its early stage, but we think marks a profound change – with implications for our asset allocation and how we can best manage risk over the course of the cycle.

Moral hazard has ceased to stand in the way of intervention. Rescuing the overindebted financial system, a development that the US Federal Reserve had overseen and in fact encouraged, came to be all that mattered. This trend became global when in 2012, the Fed’s brother central bank, the European Central Bank, dropped its emphasis on moral hazard with the promise of its Chairman Mario Draghi to “do whatever it takes” to stop the debt crisis that was threatening to bring down Europe’s financial system. So died 140 years of central banking policy. Welcome to the new world of central banking.

This change upended 140 years of central bank crisis management that Bagehot had so well described. Certainly, the Global Financial Crisis marked an important escalation in government in many aspects of the global economy and had many unintended consequences that accompanied this greater activism. One such change was that the health of our fragile financial system became more important than moral hazard. This meant ever more proactive efforts by central bankers to try to keep debts from going bad, such as their recent and powerful global response to the COVID-19 crisis. Our regulators made it clear that they did not want system-wide debt levels to fall, but rather did whatever it took so that debts would keep growing. This has many important and poorly understood repercussions that will impact financial markets for many years, not all of them good. However, we believe one thing is clear, that we can use the knowledge of how central bank behavior has changed to manage risks more thoughtfully over the course of the cycle.

Bonds: We Believe the Trend is (STill) Your Friend

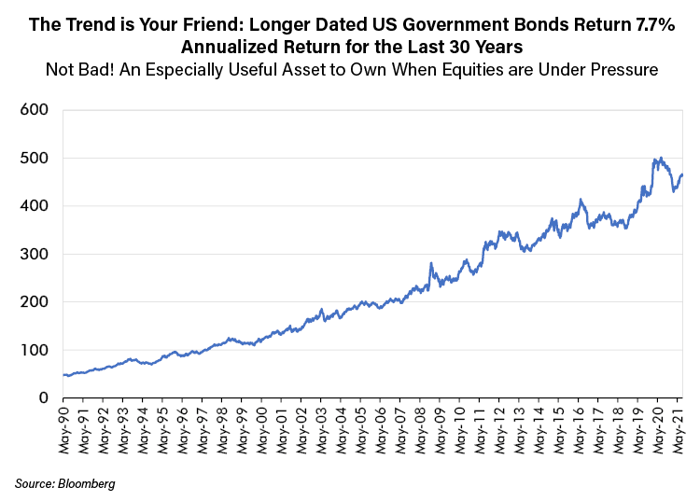

The chart below shows that the total return (yield + price appreciation) of the longest dated U.S. government Treasury bonds have been 7.7% per year for the past thirty years!

We believe this makes such bonds a good investment in their own right. Furthermore, we believe that central banks’ newfound embrace of moral hazard suggests even lower interest rates in the future, as it leads to overindebtedness which weighs upon growth. After thirty years of “stimulus,” Japan is the industrialized world’s most indebted – and slowest growing economy – with one of the strongest bond markets and thus the world’s lowest interest rates. Could this be our future?

Panic Early: Beat the Rush!

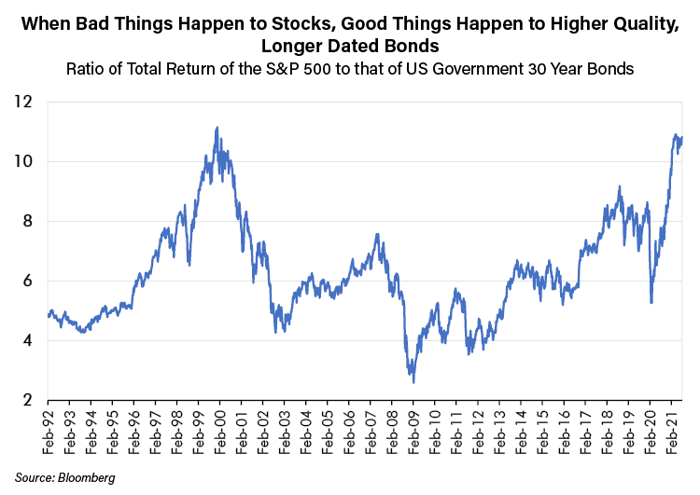

The chart below demonstrates why we think that the highest quality, longer-dated bonds can be powerful investment tools – especially when owned within an equity rich portfolio. Above we show their impressive long-term returns. However, even better, such bonds have historically tended to rise in price when equities decline. We also like the forgiving trade structure of being paid interest while we wait for bonds to perform their most needed diversification effort. This makes time our friend and not our enemy.

We think this is a superior form of risk management because it is not dependent upon perfect timing – such as remaining fully invested until the day the market peaks and then selling. If the hope of perfect timing is your risk management “strategy,” then I fear you are setting out to fail. Everyone hopes to sell at the absolute top and buy at the absolute bottom. We have found such perfection elusive. Although if you are, in fact, that rare individual who can see the future, we have a job for you! Our research team is on the lookout for clairvoyants! Failing such psychic powers, our research team has embraced a more disciplined risk management philosophy. Our goal is to try to buy these safer assets - with their valuable and diversifying return pattern - when they are most unloved and seemingly un-needed. Those times tend to be when equity markets are at new all-time highs – like now!

In Conclusion

Central banks are pulling out all the stops to encourage debt growth. But, is adding more debt really a sustainable answer to a crisis of overindebtedness? We think certainly not. However, our regulators have chosen to do just that. They have chosen this path due to their terror over the fragility of the financial system that they oversee. Why else would they have abandoned 140 years of concern about moral hazard? We believe that with this new direction our regulators have fully embraced an overindebted future and all its unintended consequences. This means, to us, higher future market volatility as future debt crises are now all but assured. Look no further than the incredible volatility of the past year as equity prices crashed then boomed if you needed a reminder on the difficulty of forecasting the future. We think a more active approach to portfolio management is required in such times. We think fast moving cycles and growing government intervention will plague our markets going forward. We also believe that central bankers have already chosen to let overindebtedness weigh on long-term growth, which should result in a future path of interest rates in the long run that are lower than almost anyone thinks. That has been the lesson of Japan. Will it be true for us as well?

In a confusing world, we try to focus on simple truths. One such truth is that debts issued now are a claim on resources in the future. So, the paradox of stimulus from debt growth is that, while its growth is initially “stimulative” in the short run, it is deleterious in the long run. For these reasons we have never been tempted to give up on our bullishness towards what we consider to be among the highest quality, longest dated bonds in the world – U.S. Treasury bonds.

We believe that the opportunistic purchase of higher quality, longer dated bonds is a smart strategy to prepare for future central bank interventions of more debt growth, lower long-term growth, and lower long-term interest rates. We believe that the best prices in the safest assets come when equity markets are at new all-time highs – like they are now. Because then few are focused on managing risks, which is exactly when risk management is the most valuable! It takes discipline, though, to pro-actively reduce risks and make investments safer when risk taking appetite is the keenest, such as now. But we believe that such discipline is the bedrock of thoughtful risk management, which is why we like to shop for our winter coats in the summer – when they are on sale!