Greece and its crumbling finances have been in the press constantly of late. The day of decision for Greece appears to be approaching quickly with the latest news that the country is raiding its IMF reserve accounts to meet its debt obligations. Greece’s economy minister recently noted that the crisis may come to a head by June, just a few days away.

In most instances this kind of constant media attention is a sure sign that the market is very far along in its job of pricing in today the future events of tomorrow. And – for Greece – this may very well be the case. I intend, however, to focus not on Greece but rather to look ahead and consider the wider contagion effects of a potential Greek default. Investors are convinced that, should Greece default upon its debts, that there will be no contagion. The market seems to be pricing in an outcome where a Greek “financial accident” would have no spillover effect on other European debtors countries, such as Spain or Italy. Is this the right view? Much depends upon getting this answer correct. In this week’s Trends and Tail Risks, I ask the question of what might happen to other major European debtors if Greece succumbs to its debt woes.

Greece: A Quick Recap of How it Came to This

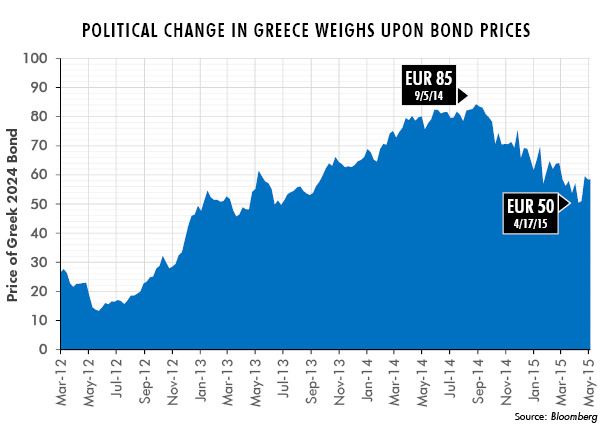

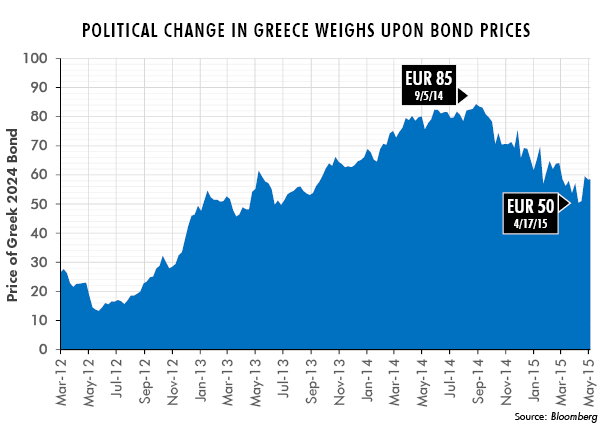

Frequent readers of this weekly will be familiar with our concern about the Greek bond market and its risk of financial contagion. In fact, next week will mark a full year from when we first started to write about our growing concerns (Big Problems Start Small, May 21, 2014). The price of Greece’s 2024 bond at the time was 77 and had been rallying for years. We saw the potential for a reversal of the favorable fundamentals that had been a tailwind for the value of Greek government debt. In particular, we noted with concern that political support was failing for the austerity policies of the Greek government. A series of local elections suggested that the market was underestimating how strongly the forces of political change could upset the balance in Greece. As is so often the case, I was early in my concerns and the price of Greek debt levitated for another four months. But the uneasy calm would not hold for long.

{kind=link}

Our study of history warned us that austerity-weary voters would have their say and kept us alert for the rise of a political backlash in Greece. Last summer we examined the example of the Invergordon Mutiny from 1932, (Ghosts of Invergordon?, June 4, 2014). In 1932 a mutiny in the English Royal Navy against deep pay cuts needed to balance the budget forced England to break its currency peg to gold. Austerity had gone too far. This political backlash was the result.

The lessons of history would serve us well. Greek voters could take only so much before the fabric of the social contract between the governed and their government started to fray. The political ground shifted in Greece to favor the rise of Syriza, the coalition of far left parties within Greece. From a price of near 85, bond prices would fall more than 40%. Greece and its debt problems went from being a non-issue to a front page economic story, where they remain to this day. What does the future hold for Greece? Our early and once contrarian concerns are now, once again, mainstream. We think a more important question should dominate the narrative now: if Greece fails will there be contagion?

Lessons of History: The Danger of Pegged Currency Regimes and the Example of Argentina

The flawed construct of the Euro is at the heart of the biggest systemic danger in Greece, and to the rest of Europe through potential contagion. The countries who have adopted the Euro did so by effectively “pegging” their currencies to the Euro. This means that they gave up the ability to change their currency values to reflect the individual country level fundamentals. No longer can these countries devalue their currencies and thus grab a greater claim on society’s resources by printing money. This currency peg creates a risk now because a major Greek financial problem could set in motion contagious forces the outcome of which few can predict. However, financial history – as always – provides many precedents for us to study, chiefly the Argentine Crisis of 2001-2002, which also involved the failure of a pegged currency regime.

The Argentine Crisis is a very useful case study to inform how we think about the ongoing Greek Crisis. Argentina initially pegged its currency to the U.S. dollar to end the vicious cycle of hyper-inflation under which Argentina had so long suffered in the 1980s. After pegging its currency to the U.S. dollar, Argentina’s economy initially boomed. Interest rates fell in a credit-driven bond rally as fears of currency devaluation subsided under the currency peg. Boom however would eventually turn to bust as debt levels soared to unsustainable levels (sound familiar?).

A long and uneasy stand-off ensued as the IMF had to step in to “rescue” Argentina many times. Austerity measures meant to shore up confidence in the value of Argentina’s debt began to bite deeply into the economy (also sounds familiar). As the economy worsened the weight of Argentina’s debt grew and grew until the market began to fear, rightly, that Argentina might be forced to end its peg to the U.S. dollar. If a currency devaluation happened, debts that Argentina owed would plummet in value as they were either defaulted upon or re-denominated in the newly devalued currency that would have to replace the failing pegged currency regime. Creditors ceased loaning money to Argentina.

These fears kicked off a self-reinforcing cycle that George Soros would call “reflexive.” Weakness fed on weakness as fear reigned. Finally, the unthinkable happened: on February 11, 2002 Argentina officially ended its pegged currency regime and in its place “floated” the value of the Peso. The Peso sank 75% in four months.

Many feared that Argentina’s collapse would spread to neighboring countries, such as Brazil. These fears proved to be unfounded. Argentina’s crisis was not contagious but rather was the tail end of a long series of financial crises in emerging markets that had begun back in 1997. However, there was one key difference between Argentina then and Greece now. In 2002 Argentina was one of the few countries in its region to operate a fixed peg currency system. Europe has many countries pegged to the Euro. Greece may soon reach the point of no return and be unable to maintain its peg to the Euro. If so, what would happen? Would contagion spread to other highly indebted European countries such as Spain and Italy? To that question we will now turn our attention. Readers who are interested in learning even more about Argentina’s tumultuous 2001-2002 debt crisis should read And the Money Kept Rolling In (and Out) by Paul Blustein, a book I recommend highly.

Is Political Risk Rising now in Other EU Debtor Countries – such as Spain? Might These Risks Spread?

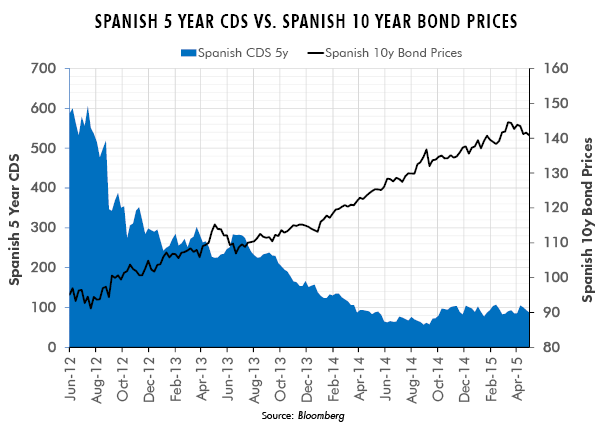

Now is the time to ask this question – while Greece is muddling along and complacency abounds. Signs of financial problems throughout Europe are almost non-existent. The graph suggests that in some obscure corners of the financial markets, however, concern is mounting.

What I find interesting about the chart above is that even while the price of Spanish 10 year government bonds have rallied, the cost to insure against a Spanish debt default in the credit default swap (CDS) market have also risen. That strikes me as strange. Perhaps this is simply an anomaly that will soon reverse. Perhaps it may mark the very first signs of investors’ fear of contagion spreading from Greece to Spain. Only time will tell for sure – but I am confident that the very sensitive Spanish debt and credit default markets will hold the clue to future events. We should monitor these markets for signs of distress in other European debtor nations as well.

Other Markets to Watch for Clues: The Relative Value of Gold

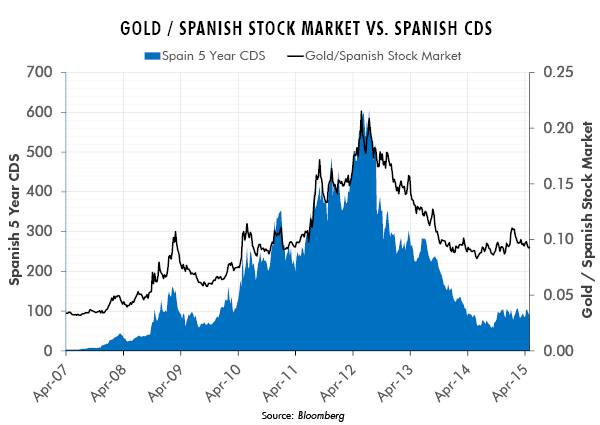

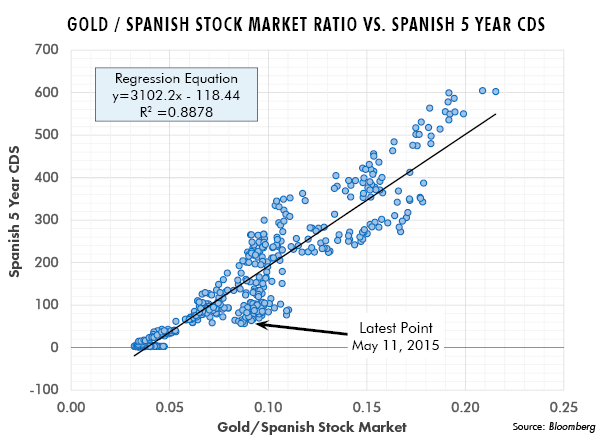

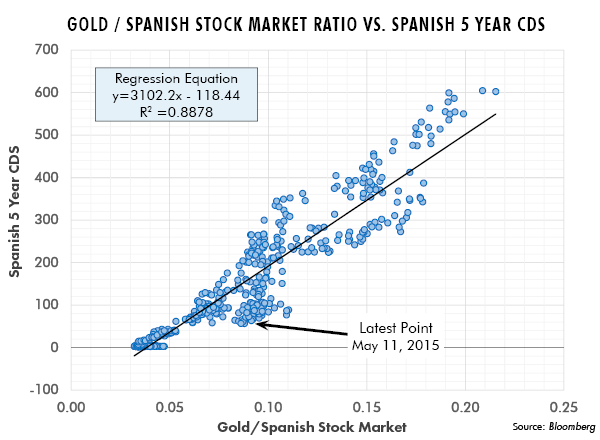

Last summer I wrote of the relative value of gold and how it moved closely with default risks (Gold: Price Versus Relative Value, July 23, 2014) and (Gold: Lessons from the Depression, August 20, 2014). The chart below defines the relative value of gold – for Spain in this example – as the ratio of the gold price divided by the price of the Spanish stock market. The chart below shows the relative value of gold in Spain moving closely with the price of default insurance on sovereign Spanish debt (CDS).

Simply eyeballing the chart shows a remarkably high correlation. Frequent readers will know that I am never content to stop at a superficial level but rather am driven to dig more deeply into the causality of why. The chart below illustrates the output of a regression analysis, a more rigorous means to quantify the fundamental relationship between the relative value of gold in Spain and CDS for Spanish government debt.

The 88% correlation between the relative value of gold and Spanish CDS illustrates a deep and timeless truth: countries may have left the discipline of the Gold Standard – but the market has not! The market is still pricing the relative value of gold as a means of protection against default. This highlights gold’s often under-estimated benefit of being an asset that is not someone else’s liability. Gold is an asset that has no default risk, and as such it becomes a more valuable holding as concerns about credit quality – and the risk of default – grow. This property of gold makes it a worthwhile investment in times of credit stress and provides us with yet another metric to monitor as we watch unfolding developments in Europe.

In Conclusion

{kind=link}

There may be much more at stake in Greece than just Greece! Now is the time to ask the question of what may transpire if Greece goes over the edge. Might investors’ concerns spill over to question the value of debts of other weak debtors in the Eurozone? If so this would lead to unexpected weakness in many European markets at a time when investors are widely exposed to them thanks to prevailing bullishness about the European Central Bank’s recent quantitative easing program. Such an event could also re-ignite the bullish consensus view on the value of the U.S dollar that until recently was so widespread.

Our quick study of Argentina suggests that even if Greece is forced to default and/or devalue its currency, contagion does not have to follow. The markets adjacent to Argentina were buffeted severely but temporarily during the Argentine crisis. Our study last summer of the Invergordon Mutiny in 1932 is also instructive and more alarming, however, because the Eurozone as a whole is operating a pegged currency system – unlike the isolated Argentine example.

Only time will tell about the future of Europe’s sovereign debt woes. But for now Spain and other countries such as Italy too should definitely be on our radar screen from now until the end of the year, when new elections must take place. Remember that it was the rise of a new political regime in Greece that focused attention on Greece’s long-festering debt problems. Let’s keep our eyes open for more of the same in the coming months in Europe. Much may depend upon it! •