Wealth cannot grow unless it is invested and therefore placed at risk. Done properly, over time, investing in the right risks can be amazingly rewarding. Choosing the right risks means avoiding the wrong risks. That sounds simple – but how do we do it? Independent research is the answer. Successful research is the engine behind successful investing. Research demands independent thought, dedication, intense curiosity and the resources to see the process through to a successful conclusion. This is why research is so challenging – and so fun!

Throughout the course of any prolonged investment campaign, the day will come when gathering clouds will threaten even the most well-designed portfolio. Fiduciaries who are charged with the shepherding of wealth through troubled times must know where to invest for safety until the storm passes.

How I Found Safety in an Unsafe World

In today’s volatile markets, it often seems to be an inescapable fact of life that no investment is really “safe” anymore. At least, not in the sense that an investment may always be safe. A more precise answer is that some investments are safe for a while. Our task as investors is to understand our world to the best of our ability, so that we may navigate it profitably.

Thankfully, not all hope is lost! History provides us with a rich store of precedents and long-term financial data that we can study to our benefit. I draw comfort during this struggle from my research and that of my analytical team. We make every effort to understand our investments comprehensively by looking far beyond what is visible to the casual observer, who only may see the surface.

When done correctly, research can lead us to profoundly powerful insights. In today’s “Trends and Tail Risks,” I share one of our most important, and I believe unique, techniques: the study of markets relative to gold (i.e. in gold terms). I think you might be surprised at its power to illuminate. The journey forward begins, as it does so often, with a better understanding of the past.

When Cash was Safe: The Simpler World of the Gold Standard

For hundreds of years much of the global economy was on some form of Gold Standard. From Sir Isaac Newton’s reforms in 1717 as Warden of the Royal Mint in England, until 1971, the yellow metal played a key role in anchoring currency values. Currency values were defined as a set weight in gold. For instance, for much of the 1800s, the price of gold in U.S. dollars was fixed at a value of $20.67 per ounce. The dollar’s value was thus “pegged” to gold. Each dollar’s value was set at a ratio where one dollar’s value = 1/20.67 of an ounce of gold. When investors sought safety, they sold their investments in stocks and bonds and “went to cash.” This meant, more precisely, that they went to gold.

So a rising cash balance then was the perfect safe investment, especially in times of credit stress when gold tends to appreciate in relative value ("Gold: Lessons from the Depression, 8/20/14") as Roy Jastram’s epic tome The Golden Constant so richly demonstrates. Let me be very clear on this point: in a Gold Standard world “going to cash” was not the lack of a bet, it was an active bet that gold’s relative value would rise against the values of what gold could buy: commodities, stocks, and bonds for instance. Going to cash was an aggressive investment in safety. So the safest investment was also the simplest!

How tragic that the world was deprived of such an elegant solution. In its place we now have anchorless currencies that move about seemingly at random. No one designed this “system” of “floating currencies,” rather President Richard Nixon thrust it upon us in 1971 as part of his desperate re-election gambit. All values are now afloat on an ever-changing sea. This infinitely complicates the job of the investor who is truly seeking safety.

Cash has no set Value Anymore

If the value of a currency is constantly fluctuating, then by definition all the values of all the assets and liabilities in these currencies are also fluctuating. Surely this creates profound limits to what we can say with precision about what anything is truly worth. Sounds confusing doesn’t it? But it doesn’t have to be that way. There is a way forward.

Honest Measurement

One of my most controversial beliefs about the financial markets is that while our political and central bank leaders took us off of the Gold Standard, the market itself remains on it. This is because gold’s behavior in market cycles is not a man-made convention, but rather gold jealously and strictly guards its own value over the long run often with insulting results! Perhaps an analogy might be useful.

For instance, I must admit to my own disappointment, when I look down at my bathroom scale, to see that I gained a few unwanted pounds this holiday season. Diet and exercise are the two most straightforward choices I could make to reverse this weight gain and eliminate my scale’s unpleasant message. Our political and central bank leaders, however, inspired by their experience of eliminating the strict measures of the Gold Standard, might suggest a different choice: let the value of a pound float!

No longer would a pound have to be defined as a fixed ratio of one pound=16 ounces but could be devalued to one pound=20 ounces! Effortlessly I could watch my weight in these newly devalued pounds fall 25%! If I am really interested in a true measure, however, I will not use such a gimmick. So too it is with measuring our financial investments.

Gold ratios display the simpler world of how asset prices would look under the rules of the Gold Standard. Gold is costly to produce, requiring a meaningful investment of both labor and capital to produce each ounce. These costs change only slowly over time which is a key part of the long-term stability of gold pricing. This is a key reason why I look at asset prices in gold terms: I want to weigh their value with an honest and unchanging scale. We can discover surprising relationships when we dare to measure the markets honestly.

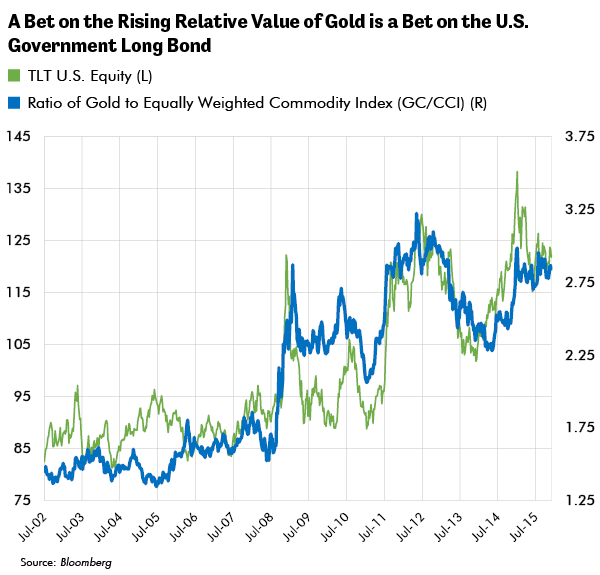

The Relative Value of Gold and the Bond Market

In the chart below I define the relative value of gold as a simple ratio of gold/commodities. A rising ratio, a rising relative value of gold, means that gold buys more commodities. It’s easy to understand why. Desperate commodity producers increase supply into a weak economy in an attempt to lower their unit cost of production. Unsurprisingly, gold buys more commodities in such an environment when the economy is depressed.

I show in the chart below the exceptionally strong relationship between the relative value of gold and the price of the TLT, which tracks the price of the most long-dated U.S. government bonds. I believe this points to a deep and highly misunderstood correlation: an investment in long-duration U.S. government bonds is the modern equivalent of “going to cash” under the old Gold Standard! An aggressive investment in safety can be achieved by investing in long-dated U.S. government bonds! Both can be winning investments in a deflationary world that suffers from overindebtedness.

This relationship is true not only for U.S. government bonds but also is applicable for the strongest bonds of the highest duration, such as extremely high quality U.S. corporate bonds. This insight has been a key cornerstone of our bond strategy, and a key driver of its success.

One powerful insight made it all possible. I confess it took me years of constant questioning and tireless research to understand this elegant truth. All of the world’s most profound insights are obvious, in retrospect. No one said that successful investing would be easy!

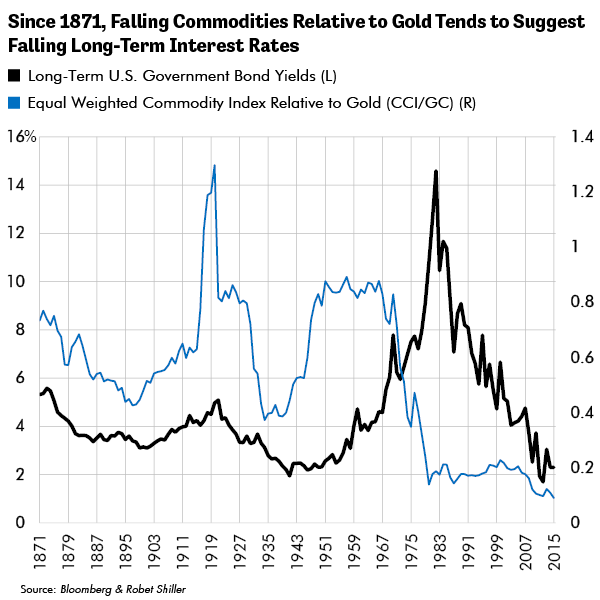

Can One Hundred and Forty Years of Data be Wrong!?

The chart below shows a longer running time series of the relationship between bonds and the relative value of gold. In this chart I display the data in a different way, looking at commodities relative to gold versus long-term interest rates. These measures tend to decline together: commodities devalue in gold terms typically during periods of falling interest rates, during a depressed economy. The full sweep of the data shows the longer-term pattern. All too often observers fixate solely upon the experience of the 1970s, which was a highly disruptive paradigm change from the Gold Standard’s pegged currency to that of a “floating” currency. History, however, is much more comprehensive than any isolated decade.

The world’s bond bears need to study this chart. If they did, they would see that there has never been a “V” bottom in these measures. The secular turn in the cycle from falling interest rates to rising interest rates has always taken decades. Furthermore, the secular turns in interest rates from down to up have all been preceded by a similar and long-running increase in the relative value of commodities versus gold. Secular bond bears may choose to ignore these clear messages of history. I will not.

In Conclusion: We Remain in Deflation– but it’s a Modern day Deflation

Mark Twain said that history doesn’t repeat but that it does rhyme. As investors, we have to understand how today’s markets rhyme with history. I believe that the evidence is pretty clear that we remain mired in a secular deflation. More than one hundred and forty years of data can help us understand long-term investments for such a world. I have examined this topic many times in this publication ("Negative Interest Rates, 2/4/15," "Is Credit Quality Peaking?, 8/6/14," "Our Bond Strategy: The Power of Duration, 10/8/14"). The U.S. long bond, and other long-duration bonds of the highest quality, can be safe instruments to own as long as the long-term environment is deflationary. These investments offer us a way to try to recreate the simplicity that our politicians and central bankers stole from us.

I wish that this were all that we needed to know to safely navigate the markets! Sadly this is not the case. Investors must also deal with the incredible volatility that central bankers now wield in the markets. Their arbitrary words and acts periodically shock the markets and threaten to overwhelm even the most thoughtful and fundamentally driven analysis. A diversified portfolio and a watchful eye on the cycle are the tools with which we attempt to navigate this volatility.

We can draw further comfort from the wisdom of Francis Bacon, who noted that knowledge is power. There can be no doubt that understanding the world in gold terms gives investors an edge through deeper knowledge. In today’s highly competitive markets, I will take any advantage I can get that helps me to find safety in an unsafe world. •