Chief Conclusion

Evidence continues to accumulate globally that the secular bull market in bonds is alive and well. We discuss the most recent data that includes Europe’s first negative yielding corporate bond (BBB- rated), failing relative performance of banks globally, and a quickly shrinking premium of U.S. government 30 year bond yields versus 5 year yields (flattening yield curve). We outline how we have our portfolio defensively positioned for this stage of the cycle, and why.

Dr. Strangelove or How I Learned to Stop Worrying and Love the Bomb

Dr. Strangelove, Slim Pickens Rides a Missile.

“Dr. Strangelove” is a wickedly absurd movie that tackled a weighty issue. Made in the wake of the Cuban Missile Crisis, the movie features a rogue military base commander launching a nuclear attack on the Soviet Union without the knowledge or approval of the President. This already serious situation escalates dramatically when the U.S. learns that the Soviets possess a “doomsday” device that will retaliate automatically with its own launch of nuclear missiles if the Soviet Union is attacked. A full cast of characters, including Peter Sellers playing three roles, culminates in the iconic image above of Slim Pickens riding a nuclear missile.

It’s a funny but dark spoof of a serious issue. You should definitely watch it if you have not yet seen it.

Recent research has shown that parts of the movie were uncomfortably closer to truth than anyone realized at the time. First, the book that inspired the movie, “Red Alert” had been researched meticulously and confirmed that such a rouge launch was indeed possible. This threat was sufficiently frightening for the Kennedy Administration to launch a sweeping overhaul of the command of our nuclear arsenal to centralize its control. Second, even more troubling, Soviet archives show the existence of a Soviet “doomsday” machine, called the Perimeter System and code named “The Dead Hand” that was completed in 1985. It was a network of sensors whose job it was to sense if a nuclear detonation took place in the Soviet Union and to automatically launch its own nuclear missiles in the event that Soviet commanders could not communicate.

Negative Interest Rates (Again)!? Inconceivable! Is Art Influencing Life?

In the financial world - the closest farcical equivalent of this movie seems to be in negative interest rates, especially in Europe. We have written about this before (Negative Interest Rates?).

Recent events have become even “stranger” with the first issuance of a negative yielding bond in Europe, not by a sovereign “risk free” borrower, but rather by a run-of-the-mill investment grade rated company.

Truth is Stranger than Fiction in the Bond Market

When there were “only” negative interest rates in European sovereign bonds, you could kind of almost wrap your head around that since there is always some demand for a “risk free asset.” But, negative interest rates for a modestly rated corporate debtor…that’s new.

It should go without saying that paying money for the privilege of bearing the real risk of not getting your money back is a really bad idea. Sovereign countries have the power of the printing press to create the means by which to satisfy their liabilities, so one can (kind of) get the whole negative sovereign bond yield thing. But to extend the same privilege to bonds with substantial, or at least meaningful, credit risk? Really?!

Passing on this “opportunity,” however, is not the same as fighting the trend. Far from it. The bond market, particularly the higher-quality, longer duration bonds that we favor, likely has a lot left in it. In contrast, the more risky, lower quality debt markets are hiding some huge problems with which we are going to have to deal with in the future. More on that later.

What I have not seen is the latest crop of bond bears address this development. Their silence is deafening. Admittedly, this year’s crop of bears is only the freshest in what has proven to be a bottomless font of talking heads calling the top of the bond market.

Two Decades of the “Widowmaker Trade:” A Brief History of Misplaced Bond Bearishness

This strange fascination that some seem to have with hating bonds began in earnest in 1998 when “amazingly low” Japanese sovereign bond yields started to plummet in earnest. Thus began the investment equivalent of the World War I bloodbath, the battle of the Somme, that claimed one million dead or wounded. The toll of that battle, and its financial equivalent, betting against bonds in the financial markets, should be a cautionary tale.

But proving that no one learns anything in the markets, the bond bears have destroyed their capital wantonly for decades now with no less relish than Europe’s misguided generals fed the flower of its youth into the maws of the machine guns. Sometime in the late 1990s, someone with a gift for phraseology termed shorting such bonds the “widowmaker.” Somehow, two decades later, it’s still appropriate.

In 1999 I remember bond giant PIMCO’s Bill Gross, the “Bond King” of the time, make a detailed and passionate call for a peak in the bond market – for yields to rise and bond prices to fall. In time, the data proved his view to be mistaken.

PIMCO reiterated this call in 2003 though I must admit that then I really thought that they had nailed it. After all, China was industrializing which led to one of the biggest inflationary commodity booms of all time. If there was ever a time for bond’s long rally to end and for interest rates to start to rise, it was then.

And then came the Global Financial Crisis.

Yields dropped further, sending the prices of higher quality, longer dated bonds soaring. I was wrong to be worried about bonds in 2003, just like all the “experts” were. The conclusion I reached in 2008 was that if the boom that we had from 2003 to 2008, including a near four-fold rise in the price of gold (at the time), was not enough to break the bond market, then there was truly something profound at work here. We must endeavor to understand it. Ten years later I am still trying. From time to time I feel like I am making progress.

I can tell you that, from my own experience trading more than one hundred cycles, a secular bull market in anything tends to continue until no one is left to fight it. With so many “experts” calling for the end of the bond bull market, we seem about as far away from that psychological capitulation as humanly possible. But let’s not rest on sentiment alone, let’s look further to see what the evidence suggests.

Focus on the Facts, Not the Legend

One way that I check in on important trends is to view them globally. When I do so below, in a quick tour of charts, I see no evidence of a change in trend in the ongoing bond bull market.

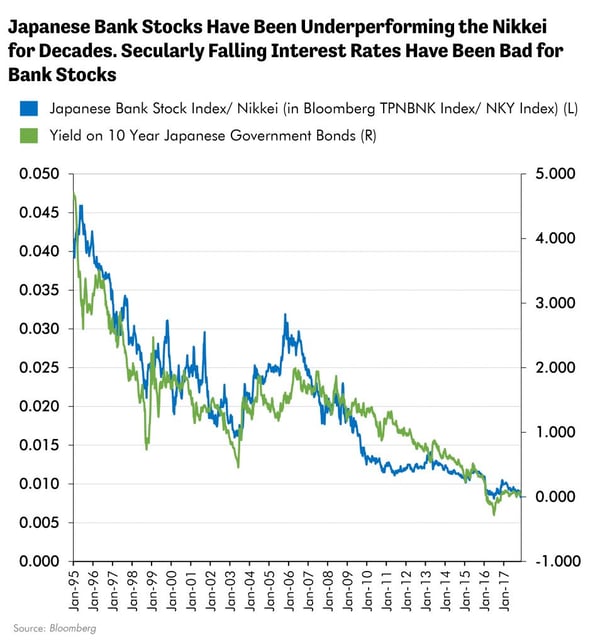

Japan is the most enduring home of secular deflation, of the bond bull market, and I see no sign of change there. In fact, one of my best indicators for bond yields in Japan has turned down, again. That is shown below in the performance of Japanese banks relative to their home stock market, the Nikkei. It makes sense that bank stocks would lead long term interest rates. I have long noted how equities tend to move in advance of their fundamentals. Because so much of a bank’s income is driven by the spread between what it charges for lending and long term interest rates, bank stocks should anticipate interest rate changes. The chart below shows this quite clearly over a more than twenty year period.

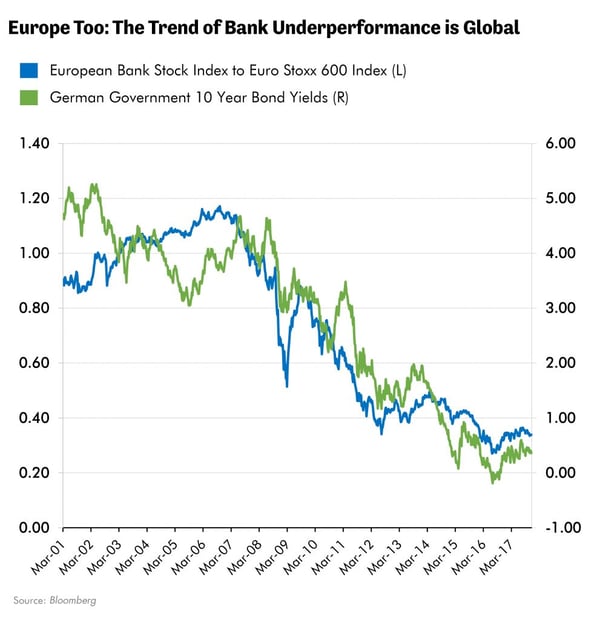

The same holds true in Europe, with European banks underperforming the broader indices, in lock step with falling German sovereign bond yields.

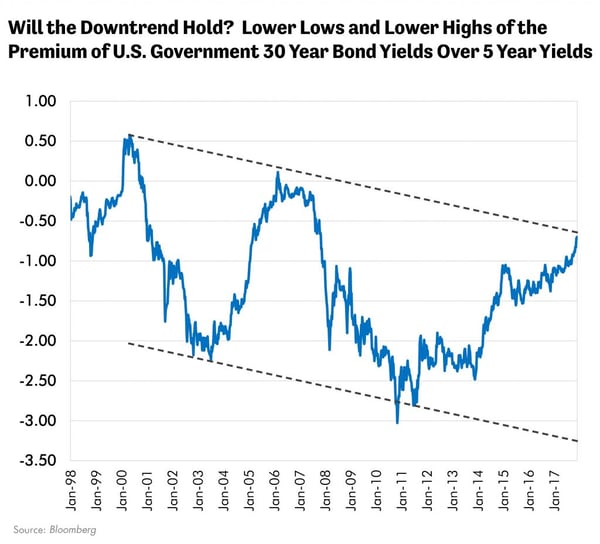

Finally, the chart below also tells a cautionary tale for critics of the bond market. It displays the secularly shrinking premium that the market demands for the U.S. government 30 year bond over yields on the 5 year bond. The fancy word for this is a “flattening yield curve.”

At some point in the cycle, higher short-term interest rates will begin to slow the economy enough such that longer-dated bonds, such as U.S. government 30 year bonds, will begin to rally as their yields fall, anticipating rising risks of a recession. No one knows when this point will be, but the chart below with its lower lows and lower highs suggests that perhaps we may be at an important juncture right now. When that line begins to move down, it will be time to make portfolios even more conservative.

But I Repeat Myself: What This Means for How our Portfolios Are Positioned

Despite near universal enthusiasm for bank stocks in today’s market, we remain underweight that sector relative to the broader indices. We do own a select few of those we consider to be the best, but otherwise we cannot muster other investors’ overwhelming enthusiasm for them as a broader asset class, given the evidence above.

We have chosen to gain our more cyclical exposure to a strengthening economy through beaten down basic materials equities. In particular we continue to find compelling values in the commodity realm, such as in fertilizers, steel, and shipping for instance, where we can own assets that trade at a deep discount to their replacement value and should see their fundamentals improve with the economy.

We continue to own, as the single biggest part of the portfolio, higher quality growth stocks. This means that they pay a growing dividend that we believe is sustainable. After all, if the market is OK loaning money for nothing to a borrower despite evident credit risk, at what multiple will the market value the world’s best companies that pay a rising dividend? Ponder that for a moment.

While you are pondering that, consider that if the market is endorsing the “return free” lending of money at a guaranteed loss to a risky corporation, then the ownership of a non-interest paying yet default free asset like gold cannot logically be a bad thing. We continue to be happy with our thoughtful exposure to gold through our targeted investment in the gold royalty industry.

In bonds this means that we continue to advocate a bias toward higher quality and longer duration holdings.

In Conclusion

If all of this sounds strangely familiar, it’s because you have heard it from us before and will likely hear it again.

Many in the markets are not tasked with the responsibility of shepherding shareholder capital through perplexing markets and thus are free to make wild predictions about future outcomes. After all, no one will remember if they are wrong, and if they are right, just think of how many newsletters they will sell!

Our task as investors is different. Our task is to construct a resilient portfolio to thoughtfully participate in an aging bull market while also prudently taking positions to limit the portfolio’s downside once this cycle inevitably ends. That’s why we construct our portfolios with a view to keeping them defensive and diversified.

Diversification - after all - by definition means that the individual holdings in the portfolio will not all go up or down together, but will have a different pattern of returns. By design this portfolio is not built to “look like the market” but rather has what we believe to be a higher level of defensiveness. We believe that, should our overindebted world stumble along the pathway to glory, higher-quality, longer-dated bonds - and gold - will be among the best performing asset classes to own. •