“When you raid a cathouse, you take the piano player too.”

-Sheriff Buford T. Justice, Smokey and the Bandit II

We always manage our investments with an eye to where we are in the cycle. That discipline is proving highly valuable in the turbulent markets of the last few weeks. Investors have (re)discovered that central banks have not been able to banish volatility from the financial lexicon - although they had managed to bottle it up for a while.

We think often about the quote above during these market downdrafts. The frustrating truth is that the most likely outcome during these “market raids” is for most equities to get drawn into the downturn (at least for a while), even the innocent piano player! We have thoughtfully researched all our holdings and don’t part with them lightly. Neither, however, do we stubbornly hold onto our positions when our research suggests that a downturn is near and we can profitably exit ahead of time while making the portfolio more defensive. We firmly believe that it’s better to be safe than sorry. In this week’s Trends and Tail Risks, we examine what markets got raided and what it all means.

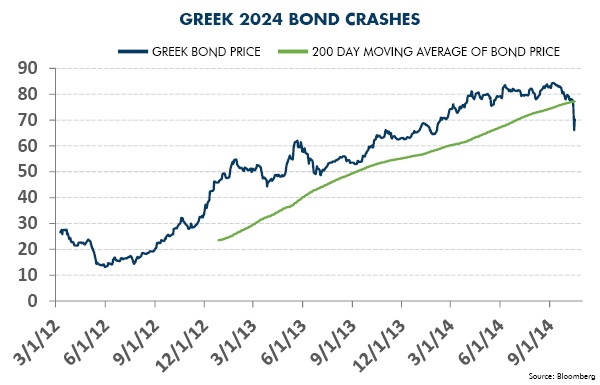

The inventory down-cycle now underway (Revisiting the Inventory Cycle, October 1, 2014) has broken the Greek sovereign bond market. Inventory destocking cycles are unexpected economic decelerations that tend to stress the credit market and often break the weakest link in the credit chain. Is the market now saying that Europe’s sovereign debt problems once again are the weak link in credit? It is too early to tell for sure but we fear that the answer may be “Yes.”

We have been writing about the Greek bond market for months (Big Problems Start Small, May 21, 2014). Our concern has been that the social contract between Greek voters and its government is fraying. The Greek politicians who voted for the Greek austerity package back in 2012 are now in big trouble. The vital signs of the Greek economy are not as bad as they used to be, but still confidence has collapsed in the politicians leading Greece. The chief opposition party, SYRZIA which stands for “The Coalition for the Radical Left” is now expected to become the largest party in Greece. Among SYRZIA’s more radical views are promises to restructure the onerous terms of the German-led bailout or even walk away from the debts that Greece has promised to repay. This is good news for the politicians of SYRZIA, who see this issue as the way to get elected, the goal of all politicians. This is not good news, however, for those who own Greek bonds, as the chart above displays.

The Greek bond market chose to ignore the first rumblings of political discontent that we first outlined back in May. Perhaps the owners of these bonds were under the spell of the promise of Mario Draghi, the head of the European Central Bank (ECB), who famously promised in July of 2012 to “Do whatever it takes” to save the Euro and its highly flawed credit system. This “promise” drove the six-fold rally in these bond prices off the lows of 2012. What could go wrong with such a promise – especially one that had been so profitable to bond holders? The underlying flaw in this thinking, now revealed, is that everyone assumed that the terms of the Greek bailout deal would hold. That assumption is now being called into question. But why now? Why not five months ago when we first highlighted this flawed assumption? The turn in the inventory cycle from restocking to destocking holds the key. It was this catalyst that revealed the flaw.

Credit Investors “Caught Leaning” in Risky Bonds by the Turn in the Inventory Cycle

Investors in the credit markets were “caught leaning” (Credit: Caught Leaning? August 13, 2014). They were “reaching for yield” by investing in risky bonds with weak credit, such as Greek sovereign bonds, in a desperate and ill-timed search for income in a low interest rate world. The more appropriate description of this activity is “picking up pennies in front of a steamroller.” It’s a practice that, while surely thrilling, we will leave to others. Our own strategy in bonds (Our Bond Strategy: The Power of Duration, October 8, 2014) could literally not be more different at this point in the cycle. Our strategy has been to take duration risk when we were paid to take it: in the last few months when everyone else was shunning it. Consensus believed that “only an idiot” would buy high quality, long duration bonds with an obviously booming economy and the Fed winding down its Quantitative Easing (QE) program. As always, that which “everyone” knows has little value.

Once again a one-sided consensus view was proven wrong. Long duration high quality bonds, such as the US 30 year bond, have now returned nearly 12% for the year! Yet those investors following the herd stampeding into many high yield bonds are now sitting on year-to-date losses.

Why do we care about Greek bond prices? Because they represent the leading edge of the greatest systematic risk in Europe – the fraying of the social contract and rising risk of sovereign default

Greek sovereign bond prices are very important for many reasons. The first is that consensus deluded itself into believing that the ECB’s promise to “do whatever it takes” had fixed all of Europe’s sovereign debt problems. The serious break in Greek bond prices reveals the flaw in that thinking. Will German public opinion allow the ECB to buy Greek debt if a new set of politicians in Greece is threatening to default on that debt? What other countries in Europe have seen their bond prices levitated by such central bank promises – promises that may now logically be questioned? The second - and more deadly – problem revealed in Greek debt is that angry voters of a sovereign nation are raising the odds of a debt default or restructuring. To paraphrase an exceptionally insightful market observer: One is an anomaly but two is a trend! We will be watching sovereign bonds of other EU countries very closely for signs of contagion, which can be so dangerous in propagating credit stress. Bond prices will fall and bond yields will rise in Greece and throughout Europe if this trend grows in strength, as we fear it will.

Misguided Policies Exacerbate Europe’s Weak Credit Fundamentals

Sadly a whole new round of credit stress in Europe may be kicking off right now. Greek banks own Greek government debt. These banks count Greek bonds as bank reserves. If you were a Greek depositor, how would you feel about the safety of your money in a bank that owned these bonds whose values are now crashing? Perhaps you would feel less safe now than you did just a week ago? Perhaps you might even be motivated to move your money to a safer bank? Or better yet perhaps even to a bank outside of Greece altogether? Even worse - what if Europe extends its “bail in” policy to troubled Greek banks, where bank depositors and creditors pay the costs of failed banks rather than taxpayers? Surely such a policy penalizes depositors and creditors who get trapped in a failed bank. Is it a sound and thoughtful policy to incentivize creditors and depositors to flee at the first sign of duress? Who could possibly think that this is a good idea? Troubled banks need more capital and more depositors, not less. In all my years of investing I have never seen a more perverse and misguided set of incentives. Future historians will look back on the enormous errors of Europe’s policy makers and wonder at their lack of foresight.

Surely many thousands, if not millions, of Greek depositors are asking themselves these questions right now. If enough of these depositors and bank counterparties and creditors decide to act upon their fears, a “reflexive” cycle of financial distress could kick in, where expectations of further weakness accelerate an already intensifying fundamental decline. As the odds of a bank’s failure rises, the incentives for a bank’s depositors and creditors to flee will rise, making it MORE likely that the bank will fail. I have seen this “reflexive” dynamic unfold many, many times. Almost everyone misunderstands how powerful and dangerous such a cycle can be. Greece, and by extension many other countries and banks in Europe, may be on the cusp of just such a move.

Will the US markets be the innocent piano player caught up in this raid? What other markets shaken in this inventory destocking cycle may also be measured and found wanting? These are the most important questions in the market today. These are the questions on which our research is focused. In the meantime, one thing is clear, we will not hesitate to think independently and act upon our views to avoid losses and find profits even during turbulent times.•